Federalism and the End of Obamacare

abstract. Federalism has become a watchword in the acrimonious debate over a possible replacement for the Affordable Care Act (ACA). Missing from that debate, however, is a theoretically grounded and empirically informed understanding of how best to allocate power between the federal government and the states. For health reform, the conventional arguments in favor of a national solution have little resonance: federal intervention will not avoid a race to the bottom, prevent externalities, or protect minority groups from state discrimination. Instead, federal action is necessary to overcome the states’ fiscal limitations: their inability to deficit-spend and the constraints that federal law places on their taxing authority. A more refined understanding of the functional justifications for federal action enables a crisp evaluation of the ACA—and of replacements that claim to return authority to the states.

The election of Donald Trump and an ascendant Republican majority in Congress may mean the end of the Affordable Care Act (ACA), better known as Obamacare.1 As of this writing, Republican efforts to repeal and replace the ACA have become mired in an intraparty fight between hardliners who favor outright repeal and moderates concerned about ripping insurance away from millions of people. But talks among Republicans continue, and the political situation remains fluid. Only time will tell.

As the debate over health reform continues to rage, one question that is likely to emerge—indeed, it has already emerged—is why national reform was ever thought necessary in the first place. At the core of our federal system is the principle that the states should take the lead unless there is a need for national action.2 Federalism is said to foster political participation, to enable experimentation, and, especially, to allow states to tailor their laws to better suit the preferences of their citizens.3 Yet the progressive push for universal health coverage has had a doggedly national focus. Even Republican repeal-and-replace proposals stop well short of a total devolution to the states. Why?

Purely as a strategic matter, the emphasis on federal law needs some defense. By way of comparison, consider same-sex marriage. When Massachusetts eliminated its prohibition on same-sex marriage in 2003, advocates did not turn immediately to the Supreme Court. They built the groundwork for a national strategy by winning in state courts and state ballot boxes. By the time the Supreme Court decided Obergefell v. Hodges,4 thirty-seven states allowed same-sex marriage, most through judicial decisions but eleven through referendums or legislation.5 Contrast that to universal health care coverage, where the score was a lopsided forty-eight to two, with only the deep-blue states of Massachusetts and Hawaii offering near-universal coverage.6 Perhaps the states’ collective failure to achieve near-universal coverage indicated the shallowness of public support for health reform. Perhaps the progressive commitment to a national solution was premature.

This federalism narrative has taken hold among health reform’s opponents. It was the cornerstone of the two constitutional challenges in National Federation of Independent Business v. Sebelius: petitioners argued both that the federal government lacked the power to adopt an individual mandate and that the states were being unconstitutionally coerced into expanding their Medicaid programs.7 It underwrites much of the hostility to the “federal takeover” of the health-care system. And it lends force to Republican proposals to return power over health reform to the states. As Speaker of the House Paul Ryan explains in his blueprint for replacing the ACA, the states “should be empowered to make the right tradeoffs between consumer protections and individual choice, not regulators in Washington. The federal role should be minimal and set a few broadly shared goals, while state governments determine how best to implement those goals in their own markets.”8

As with so many paeans to federalism, political opportunism explains much of this state-centric rhetoric. But there is much to be said for the argument that the states should take the lead on health reform. Jerry Mashaw and Ted Marmor argued as much back in 1996, fresh off the defeat of President Clinton’s health reform bill. “There is unlikely to be any single system that either is or appears ‘best’ for the whole of these United States,” they argued. “Regions, states, even localities, differ in their demographic characteristics, political cultures, existing styles of medical practice, and appetites for medical services. What is both practical and desirable varies enough to make federalist variation both normatively attractive and politically wise as an alternative to national stalemate.”9 Why not let the states make the hard calls about whether and how they want to tax their residents to finance insurance for those who lack coverage by dint of poverty, misfortune, or irresponsibility?

For those who believe in the functional virtues of devolution, that’s a challenging question—more challenging than the ACA’s supporters generally admit. As I explain in Part I, the traditional arguments in favor of a national solution have little resonance for health reform. Federal action is not needed to forestall a race to the bottom; states that decline to expand coverage impose no costs on other states; and states are not afflicted with political pathologies that might justify national intervention.

Yet for all that, a national solution was appropriate—even necessary. As discussed in Part II, two features of the health system make it difficult or impossible for those states that support universal coverage to achieve it on their own. First, the states do not have the same fiscal capacity as the federal government. Because they are prohibited by law from deficit spending, they are understandably leery of adopting countercyclical obligations that would force tax increases or spending cuts in the middle of the next recession. Second, a federal law—the Employee Retirement Income Security Act of 1974 (ERISA)—bars states from adopting the most expedient laws to expand coverage. Taken together, these legal obstacles will frustrate state efforts to achieve near-universal coverage. For health reform, the federal government really is the only game in town.

Part III draws on this more nuanced understanding of the need for national health reform to examine critically how such reform ought to allocate responsibilities between the states and the federal government. Roughly, the states should retain control over regulation while passing to the federal government responsibility for money—the taxes and spending necessary to finance reform. In so doing, the argument exploits the distinction, emphasized most powerfully by David Super, between fiscal and regulatory federalism.10 Evaluated against that baseline, the ACA is a mixed bag: it properly assumes control over money but also wrests more regulatory authority from states than necessary.11 At the same time, the leading Republican replacement plans are insufficiently sensitive to the states’ fiscal constraints and to their circumscribed taxing power. Unless the plans are revised, we may see the elimination of a federal solution combined with the retention of substantial obstacles to state action—or even the creation of new obstacles. In that event, the federalism narrative should be seen for what it is: constitutional rhetoric that masks a refusal to allow any level of government to achieve near-universal coverage.

I. the traditional justifications

Federal legislation is often considered necessary, first, to avoid a collective-action problem; second, to prevent states from imposing externalities on other states; or third, to correct for a political pathology at the state level. None of these justifications is adequate to support national health reform.

A. Collective-Action Problem

To the extent that the states cannot be excluded from the enjoyment of collective goods, they will be tempted to contribute little or nothing to the production of those goods. They will prefer, instead, to free ride on the contributions of other states. Since every state has the same incentives, contributions toward that collective good will fall short of what the states, acting in concert, would prefer. Federal action may be necessary to avoid a race to the bottom.

When it comes to health reform, a race to the bottom might develop if a state’s adoption of a coverage expansion led sick people to flock to the state.12 To avoid becoming a “welfare magnet,” individual states might decline to expand coverage, even if they would happily expand coverage if they could confine that coverage to their own residents.

But the welfare magnet story justifies federal intervention only if lots of sick people move to get health insurance. The evidence suggests they do not. In a 2014 study, Aaron Schwartz and Benjamin Sommers examined migration patterns in response to Medicaid expansions in four states.13 They found “no evidence of significant migration effects” and could “rule out net migration effects of larger than 1,600 people a year in an expansion state.”14 A similar 2016 study by Lucas Goodman used a broader sample and estimated that “the migration effect of Medicaid is very close to zero.”15 These findings, which accord with other research on interstate mobility,16 make intuitive sense. People don’t lightly move17 and they rarely do so for health reasons.18 Lower-income people in particular may not have the resources or the job flexibility to pull up stakes. If people don’t move to get insurance, there is no race to the bottom for federal action to forestall.

B. Externalities

Federal intervention may be warranted where one state’s actions impose costs on other states. A state might, for example, locate smokestacks on its downwind border in order to send its pollution to a neighbor. A federal response may prevent states from passing on the costs of their productive activity to other states.

But externalities cannot justify federal health reform. If New York declines to adopt near-universal coverage for its residents, it is hard to see how that imposes costs on Connecticut or New Jersey.19 The country can easily accommodate a patchwork of state insurance laws. Indeed, it already does. In the McCarran-Ferguson Act of 1945, Congress clarified that the states—not the federal government—retain primary responsibility for regulating their insurance markets.20 Over the past seven decades, the states have adopted widely varying rules governing health insurance.21

C. Political Pathologies

Federal authority is sometimes justified as an effort to correct for political pathologies at the state level. The Voting Rights Act and other laws adopted pursuant to the Reconstruction Amendments, for example, reflect the fear that elected officials and voters in many states, especially in the South, will be systematically inattentive to the interests of minority groups.22 Perhaps federal control can assure that discrimination does not deprive those groups of a fair shot to make their voices heard.

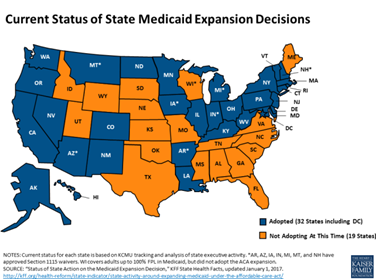

It is perhaps possible to build a similar case for health reform. In 2013, only 13% of the non-elderly white population in the United States lacked health coverage, compared to 21% of the black population and 32% of the Hispanic population.23 Although the ACA afforded the states an opportunity to alleviate those disparities by expanding their Medicaid programs, nineteen states have refused to expand. In conventional economic terms, this resistance is inexplicable: the federal government will pay 100% of the costs of expansion in the early years, dropping to 90% by 2020.24 States are passing up billions of dollars in federal money financed, in part, by taxes on the states’ own residents. What’s more, Medicaid expansion boosts employment in the health sector, enables states to reduce spending on mental health services, and raises tax revenue by redirecting the consumption of low-income people toward goods that are subject to sales taxes.25

figure 1.

What explains, then, the resistance to Medicaid expansion? Although opposition may speak to the states’ principled objections to health reform, it is difficult to ignore that the states with the darkest history of racial discrimination have resisted most staunchly. As Mark Hall has argued:

This degree of pitched opposition by states to a major federal domestic initiative has not been seen since the civil rights era of the 1960s. Then, too, states opposed federal intervention (for integration) based on states’ rights principles. But, the true motives were patent. It is certainly possible that similar motives are among the mix of sentiments shared by at least some opponents of Medicaid expansion . . . . [Coverage] disparities suggest that politicians who oppose Medicaid expansion will do more damage to their black than their white constituencies.26

If racism has tainted states’ decisions pertaining to the post-ACA Medicaid expansion, that same racism might likewise have impeded the adoption of near-universal coverage at the state level. If so, the Medicaid example might be taken to offer evidence of the need to nationalize health reform—to take the decision out of the hands of states that cannot be trusted to make it fairly.

But the case is harder to sustain than it may at first appear. State decisions about health reform may be inflected by insensitivity to minorities’ interest, but the same can be said in many other policy domains. Take education, for example. Many states can (and do) rely on property taxes to finance local schools. Wealthier communities get well-funded schools; poor and minority communities do not. Appalling as that may be, it is generally not thought sufficient to warrant a federal takeover of public schools.27 If it were, lingering discrimination would be reason enough to oust the states of their authority to tax and spend, spelling the end of federalism in any meaningful sense of the word. That kind of all-purpose justification is in serious tension with a constitutional system that remains committed to federalism, however imperfectly.

The moral case for guaranteeing universal access to care makes it easy, rhetorically, to characterize health insurance as a right—one so embedded in shared national values that the federal government ought to protect it.28 Reasonable people, however, hold divergent views about the strength of that moral case. And it’s hard to explain why, in a nation committed to federalism, the moral views of voters in one state should carry the day in another state that doesn’t see the problem the same way. Insisting that a federal law advances national values may be code for saying that some states have bad values.

For an analogy, imagine the federal government were to ban smoking in restaurants and bars, as many municipalities have done. Such a ban would be a boon for public health, perhaps more so than health reform itself. It would address fears that states were callous about the health of minorities and the poor, who smoke at relatively high rates. And a ban could be defended on the ground that it’s consistent with national values or that everyone has a right to a smoke-free environment. For all that, however, the case for federal action is weak: it depends, at bottom, on the view that the states without smoking bans have not properly weighed the public health benefits against the distastefulness of state control. The right to health insurance is closer to the right to a smoke-free workplace than it may at first appear—at least until money comes into play.

II. better justifications

For health reform, the weakness of the conventional justifications for federal intervention presents a puzzle. Why were supporters of health reform so committed to a national solution? Why did the possibility of leaving reform to the states seem hardly to arise?

There is, in fact, one very good reason for pursuing national health reform: money. State governments have neither the fiscal capacity nor the freedom to tax that the federal government does. That puts states in a bind: they cannot act even if they would prefer to adopt universal coverage and even if they are willing to tax their residents in order to do so. As the dismal history of state-level reform suggests, the states can’t go it alone.29

A. The Countercyclical Trap

In their attacks on the ACA, Republicans take aim at the federal regulations that, in their view, stymie the market, inflate the costs of health insurance, and limit consumer choice. But framing the ACA as a regulatory incursion obscures that it is not only—not even primarily—a regulatory statute. True, it creates a comprehensive suite of new rules for the (relatively small) individual insurance market. It also imposes some new rules (not many) on employer-sponsored plans. But what the ACA chiefly does is distribute tax revenue to the poor and near-poor to finance insurance coverage. The distribution comes in two main forms: first, through the Medicaid expansion, which benefits those below or near the poverty level; and second, through the subsidies available to those buying coverage in the individual market who make less than four times the poverty level. The regulations imposed on the individual market were thought necessary to assure the health of that market and to protect consumers, but they were in an important sense incidental. While the ACA does do a fair amount of regulating, it is mainly a spending program—and a large one at that.

The ACA is also a countercyclical spending program.30 When a recession hits, many people will lose both their jobs and their employer-sponsored coverage. The ranks of those eligible for Medicaid and for ACA subsidies will predictably grow, leading to larger federal outlays. At the same time, the economic downturn will depress tax revenues. The federal government can deficit-spend to manage these countercyclical fluctuations. The states, however, cannot. With the exception of Vermont, the states are legally obliged to balance their budgets every year.31 And states are understandably reluctant to adopt large obligations that will require savage spending cuts or hefty tax increases when times get tough. Cuts and taxes are not only unpopular, but they would also depress the economy further, exacerbating the recession. Broad coverage expansions thus commit states to an economic policy that could inflict serious damage on their residents.32

As the exception that proves the rule, Massachusetts is instructive. When it adopted statewide reform, Massachusetts had two advantages that no other state had. First, it had the lowest rate of uninsured in the country, meaning that its countercyclical obligations would be more modest than those of other states.33 Second, with the help of Senator Ted Kennedy, the state got a sweetheart deal from the George W. Bush Administration offering it more than $1 billion in Medicaid funding to support a coverage expansion.34 Massachusetts could afford to bite the bullet. States without those advantages cannot—at least without help from the federal government.

B. Federal Limits on State Tax Authority

A state that wishes to expand coverage can always ask its taxpayers to foot the bill. But many of those taxpayers will complain, with some justice, that it’s unfair to ask them to bear the whole burden. A resident who gets health coverage through her job—let’s call her Anna—already faces a reduction in take-home pay commensurate with the value of that coverage. Another resident who works at a similar job but does not get health coverage—let’s call him Bob—likely receives higher cash wages. Should Anna and Bob both face the same new tax, even if it finances a coverage expansion that will only benefit Bob?

From the state’s perspective, it is both easier and more equitable to adopt a law penalizing businesses that fail to offer insurance. These pay-or-play laws have a clear political logic: employers should live up to their end of the social bargain. They have a certain economic logic, too: if Bob starts getting coverage because of a pay-or-play law, he will see an offsetting wage reduction. Bob will thus “pay” for his own coverage, reducing the need for a tax increase that would also hit Anna.

The trouble is that ERISA preempts state laws that “relate to any employee benefit plan,” including a plan offering health coverage.35 Although there is some legal uncertainty—more on that in a moment—preemption probably means that states cannot impose a penalty on employers that refuse to offer health coverage.36 By taking pay-or-play laws off the table, ERISA makes it much harder for states to achieve near-universal coverage.37 And because of the intensity of the business lobby’s resistance to limiting ERISA’s preemptive scope,38 Congress is very unlikely to amend the law to address the concern.

Why might a pay-or-play law “relate to” employee-benefit plans within the meaning of ERISA? In Retail Industry Leaders Ass’n v. Fielder,39 the Fourth Circuit examined a Maryland law requiring companies with more than 10,000 employees in the state to devote at least 8% of their payroll toward health coverage or pay the equivalent as a tax. By design, the law applied only to Wal-Mart, which had come under fire for shunting its employees onto Medicaid.40 Any taxes that Maryland collected would be deposited in a specified health fund to support health coverage for Maryland residents.

The Fourth Circuit started with first principles. Under ERISA, Maryland could not direct Wal-Mart to offer health insurance. That sort of law would “relate to” the design of an employee-benefit plan within the meaning of ERISA.41 By extension, the court reasoned, Maryland could not achieve the same result by taxing a company’s failure to offer health coverage. The court brushed aside Maryland’s objection that the statute left the employer with a choice about how to structure its employees’ benefits:

Healthcare benefits are a part of the total package of employee compensation an employer gives in consideration for an employee’s services. An employer would gain from increasing the compensation it offers employees through improved retention and performance of present employees and the ability to attract more and better new employees. In contrast, an employer would gain nothing in consideration of paying a greater sum of money to the State. Indeed, it might suffer from lower employee morale and increased public condemnation. In effect, the only rational choice employers have . . . is to structure their ERISA healthcare benefit plans so as to meet the minimum spending threshold.42

The Fielder court’s reasoning is not unassailable. Rick Hills, for one, has written persuasively about why an expansive view of ERISA preemption should be rejected.43 Even with the utmost sensitivity to state interests, however, the core of the Fourth Circuit’s decision appears sound. If ERISA prevents a state from demanding that employers provide health insurance to their employees—and it does, at least under current case law—it should likewise prevent a state from imposing a substantial penalty on employers that choose not to.

The Ninth Circuit seemed to acknowledge as much in Golden Gate Restaurant Association v. City and County of San Francisco,44 even as it distinguished Fielder in a somewhat strained effort to uphold a municipal pay-or-play ordinance. For the Ninth Circuit, distinctive features of the San Francisco ordinance left employers with “a meaningful alternative” to restructuring their employee-benefit plans.45 In particular, any tax penalty paid under the San Francisco ordinance would go toward a public program dedicated to residents whose employers did not offer health coverage. In the Ninth Circuit’s view, that gave employers a real choice: they could offer coverage directly (as a fringe benefit of employment) or indirectly (via an earmarked tax).46 An employer that chose the latter approach would have to make no changes at all to its employee benefit plan. As such, the court reasoned, ERISA did not preempt the ordinance.47

The Ninth Circuit’s decision was controversial.48 Unsurprisingly, the ensuing petition for certiorari argued that the court had opened a split with the Fourth Circuit. By the time the Supreme Court called for the views of the Solicitor General, however, President Obama had taken office—and by the time the brief was submitted, the ACA had been enacted.49 Because the ACA “significantly reduces the potential that state or local governments will choose to enact health care programs” like the San Francisco ordinance, the Solicitor General recommended that the Court decline to hear the case.50 The Court obliged,51 leaving the tension between the Ninth and Fourth Circuit decisions unresolved.

For all practical purposes, the resulting state of affairs gives the states little room to maneuver. The apparent circuit split notwithstanding, ERISA almost certainly preempts pay-or-play laws that impose substantial taxes on employers, at least where those taxes are not earmarked for use of particular employees. States could minimize the risk of preemption by limiting the size of the tax penalty; as Amy Monahan has argued, a small penalty arguably leaves employers with a real choice about whether to offer coverage.52 That was Massachusetts’s approach: it levied a small pay-or-play tax of $295 per employee.53 But a small tax does little to encourage employers to offer insurance or to finance a coverage expansion—and even a small tax might still be subject to preemption. Alternatively, states could undertake the cumbersome, complex task of creating public health plans for employee use. Per Golden Gate, pay-or-play laws that earmark employer contributions might avoid ERISA preemption.

But they probably wouldn’t. Even if the presumption against preemption has purchase in other corners of the law, it does not appear to move the Supreme Court in ERISA cases.54 Without the motivating force of that interpretive presumption, it is difficult—not impossible, but difficult—to defend the Ninth Circuit’s heroic effort to save the San Francisco ordinance from preemption. Perhaps more to the point, the vote line-ups in Fielder and Golden Gate suggest that judges are split over the scope of ERISA preemption along predictable political lines. Conservative judges, with their sensitivity to business interests, tend to take an expansive view of ERISA preemption, even as liberal judges resist construing ERISA to curtail states’ regulatory authority. With President Trump’s victory and Judge Gorsuch’s confirmation, the Supreme Court probably will not be receptive to creative efforts to avoid ERISA preemption.55 At a minimum, the unsettled scope of ERISA preemption will give states pause. Why take the political hit for imposing a new “employer mandate” when the courts will probably invalidate it anyhow?56

Here, Hawaii is the exception that proves the rule. The central feature of Hawaii’s success in achieving universal coverage is a stringent pay-or-play law.57 That law, which predated ERISA, remains on the books only because Hawaii persuaded Congress to grant it an explicit carve-out from ERISA preemption.58 Lacking a similar carve-out, the other states will have an exquisitely hard time moving forward with reform. To put it bluntly: anyone who says the states can expand coverage on their own doesn’t understand ERISA.

* * *

National health reform does not resolve a collective-action problem; it mitigates no externalities; and it is not an answer to state-level political pathologies. It is nonetheless readily justified as a response to the states’ limited fiscal powers and ERISA’s sweeping displacement of state law. Taken together, these obstacles will impair the states’ ability to enact and sustain efforts to cover the uninsured.

III. implications for reform

A more refined understanding of the functional justifications for federal action yields insight into how to allocate responsibility over health reform. It also enables a crisp evaluation of the ACA and the merits of reform proposals that purport to return authority to the states.

A. The Affordable Care Act

The discussion of collective-action problems, externalities, and political pathologies suggests the difficulty of justifying federal control over the regulation of insurance. At the same time, the federal government’s superior fiscal powers must be enlisted to make coverage expansions possible. That implies a rough allocation of responsibility. The federal government should finance the bulk of any coverage expansion that commands support in Congress, but the states should retain substantial authority to structure their health-care markets as they see fit.

As always, there are federalism costs to making a collective decision about taxes and spending. Nebraskans, for example, may bridle at federal tax hikes that are used to finance a coverage expansion that they wouldn’t choose for themselves. But the alternative is worse: because of the countercyclical trap and ERISA preemption, all the states are disabled from acting alone, even if most would prefer to bear the costs that addressing the crisis of the uninsured would entail. Financing coverage at the federal level will not suit all the states, but it will suit more Americans than no solution at all.

In many respects, the ACA embraces this allocation of federal-state responsibility. The Medicaid expansion, for example, is financed almost entirely by the federal government, but states retain operational control over the program.59 The Obama Administration’s willingness to grant broad Medicaid waivers has allowed the states to adopt policies that align with their interests. Similarly, subsidies for individual plans purchased through the health-care exchanges come out of federal funds, even as states were given the option of running the exchanges themselves.60 Most dramatically, the ACA authorizes states to seek waivers from most of the statute’s regulatory restrictions if the state can show how it will use federal money—both Medicaid and subsidy dollars—to achieve the same level of coverage. If a waiver is granted, that money passes through to the state directly.61

In other respects, however, the ACA takes a heavier hand. All insurers are prohibited, for example, from refusing to cover someone with a preexisting condition.62 They must write insurance for all comers.63 They must charge the same rate to everyone, with limited exceptions for differential pricing based on age and smoking habits.64 And they must cover a comprehensive roster of benefits and cap their customers’ out-of-pocket spending.65 These are all perfectly reasonable policies, but they are not policies that the states uniformly endorse. And while states that wish to opt out of the insurance regulations can seek a waiver, the conditions on receipt of the waiver are stringent: the state plan must cover at least the same number of people with insurance that is at least as comprehensive and affordable as the insurance available under the ACA.66 Unsurprisingly, only one Obamacare waiver has been granted so far. It went to Hawaii, and it was modest in scope.67 No waiver has been issued to red states that want to depart more dramatically from the ACA’s rules.

The states thus have some reason to complain (though less than they sometimes assert) that the federal government has inhibited their lawmaking powers without adequate justification. Take the prohibition on charging older people more than three times what younger people pay for coverage.68 In its absence, the young would pay less for their coverage and the old would pay more. Maybe that’s sensible, maybe it’s not: it depends on a value judgment about how to fairly allocate health-care costs across a population. Why not leave that judgment to the states?

To push the point harder, consider the ban on medical underwriting. The ACA reflects the judgment that it is unfair to deny coverage to the sick or to ask them to pay more for their coverage. The ACA thus embraces policies—in particular, the much-maligned individual mandate—that its drafters thought necessary to cope with the risk that people will wait until they got sick to purchase coverage. For the ACA’s supporters, the individual mandate is a reasonable price to pay to prevent discrimination against the sick. But many people don’t see it the same way. Some reject the claim that the government should be in the business of guaranteeing coverage for everyone.69 Others don’t think that medical underwriting, however distasteful, warrants a heavy-handed purchase obligation.70 And still others doubt that the mandate is strictly necessary to prevent adverse selection.71 If those who disagree with the ACA’s approach command the levers of political power within a state, why shouldn’t those states be allowed to try something different?

The argument can be generalized to most of the ACA’s insurance reforms. And I can already hear the response from adherents of a national solution: Because this “something different” will not work. The ACA’s opponents are completely unrealistic about the tough tradeoffs that health-care policymaking entails. Millions of people could lose coverage.

That might be right; indeed, I suspect it is right. But that is my judgment. Lots of smart people do not share that judgment. And if federalism means anything, it is that national judgment should not supersede state judgment, absent a good reason for federal intervention. Yes, federal money might be squandered in a state that adopts stupid insurance rules. People could go bankrupt and even die as a result of the lack of coverage. But that’s an issue between the state and its voters. If other states use the money more effectively, the state with the stupid rules will come under pressure to improve them. And what if it turns out that what seemed stupid is not so stupid after all?72

Democracy rests on the conceit that we all have an equal voice in determining what the good is, which is why Michigan voters don’t get to tell Ohioans how to spend their tax dollars, even if Wolverines know in their hearts that they make better decisions than Buckeyes. And while the federal government can make decisions for Ohio, it should not do so just because it doubts the wisdom, intelligence, or values of Ohio residents. “The states have bad ideas” is a poor justification for federal law (unless, again, those bad ideas turn on views about the inferiority of minority groups). Federalism thrives when we recognize the limits of what we know, appreciate that good people can hold views that many others find repugnant, and acknowledge that our own misconceptions and prejudices can blind us. Sometimes federalism means letting the states wave their crazy flags.

At the same time, however, Congress can and should place conditions on the money it disburses to states. The possibility that a state might abuse unrestricted funds could make it difficult to enact and sustain federal legislation—which would be especially unfortunate in a domain like health reform, where the states are disabled from acting on their own. If Congress imposes new taxes to finance a coverage expansion, only to watch Iowa use that money to subsidize corn farmers, Iowa’s actions could imperil a policy of health reform that, collectively, the American public supports. Policymakers are justified in taking that political risk into account and creating broad conditions on the use of funds.

More than that: Congress can establish guardrails to prevent states from subverting the purposes of federal action, only to then use the failure of the federal initiative as an excuse to lobby for its dismantlement.73 Mashaw and Marmor propose, for example, requiring states to use federal money to achieve universal, comprehensive, portable health coverage while establishing a plan for accountability and fiscal viability.74 In other words, states should be obliged to use federal money to create an entitlement to health insurance—no lotteries or queuing permitted—but the entitlement should be articulated at a high level of generality and implemented in a manner that gives the states room to adopt their own distinctive approaches.75 The states would thus exercise authority—what Abbe Gluck aptly calls “federal-law-granted” powers—within a broad domain demarcated by Congress.76

B. Replacing Obamacare

Although it has so far failed to do so, the new Congress still hopes to repeal the ACA and replace it with a law that will return power to the states.77 If Congress wishes to give the states genuine flexibility, however, its adoption of an Obamacare replacement must be sensitive to the features of the health-care system that have frustrated state action in the past.

1. Regulation

For health reform, the most challenging federalism questions arise with respect to Medicaid and the private insurance market, where the lines of federal and state power are blurry, shifting, and contested. It is those aspects of the ACA that are the focus of the new Congress’s repeal-and-replace strategy—and the ones that can be usefully evaluated in light of Speaker Ryan’s professed aim to “empower[]” the states.78

Although replacement proposals are still on the drawing board, broad commitments have been sketched out.79 Some of those commitments advance federalism values. Republican legislators object, for example, to portions of the ACA requiring insurers to cover “essential health benefits.” They would prefer to allow insurers to cover a narrower roster of benefits, which would in turn enable consumers to shop for insurance that is tailored to their needs and pocketbooks. There are reasonable policy objections to the approach: that expansive plans will attract sicker customers, fueling adverse selection and driving up premiums for everyone; that insurance is such a complex financial product that consumers shouldn’t have to worry that their plans exclude services they might one day need; and that the coverage requirements are not that onerous anyhow. But these are also the sorts of policy objections that the states can reasonably disagree about.

The same holds true for most of the ACA’s insurance reforms, including the obligation to cover preventive services, age bands, and the ban on medical underwriting. It even applies to the individual mandate. Recognizing that stable insurance markets require a balanced risk pool, Republican legislators have been exploring alternatives. One approach, reflected in the House leadership’s preferred replacement bill, the American Health Care Act (AHCA),80 would allow medical underwriting only for those people who do not maintain “continuous coverage.” The hope is to encourage healthy people to come into the insurance market before they get sick.81 Another alternative would automatically enroll people in an insurance plan, but leave them free to opt out if they choose to do so.82 Through sheer inertia, healthy people who might not have taken the trouble to enroll might stay insured. It is not clear whether either of these proposals would be adequate to foster healthy insurance markets (or whether auto-enrollment is technically feasible). But that is the point: it is not clear. And even if the individual mandate works better than these alternatives, many people might reasonably prefer a less-effective alternative that doesn’t involve a heavy-handed government mandate. Again, given the diversity of opinion, decentralization seems appropriate.

Were it inclined to do so, Congress could adopt a baseline—perhaps the current ACA—while at the same time leaving the states free to adopt alternatives that met loose congressional benchmarks. That way, if Connecticut wanted to stick with the ACA’s regulatory approach, Connecticut could do so.83 Arkansas, in contrast, could experiment with (say) a continuous coverage provision and high-risk pools. An approach that deferred to state choice in this manner would usefully restore power to the states.

At the same time, however, some Republican proposals would impair state authority. Most significantly, President Trump ran for office on a vow to allow the cross-border sale of health insurance.84 Proposals to that effect are in most Republican plans.85 If adopted, they would allow the residents of one state to purchase health insurance that is licensed and regulated in another state.

To enable cross-border sales, Congress would have to strip the states of their authority, confirmed under the McCarran-Ferguson Act, to regulate insurance sold within their borders.86 States would be left with the residual power to oversee those insurers that are domiciled within the state. Given the ease of changing corporate domicile, insurers may move their headquarters to jurisdictions that with permissive insurance regulations. The same dynamic has already played out with credit card regulation, which is why your credit card bills come from South Dakota. Far from avoiding a race to the bottom, federal law would create one.

As a result, a state with permissive health insurance regulations—maybe North Dakota this time—could effectively establish insurance rules that govern in every other state. Voters in California and New York would have no say in the matter, even if they preferred consumer protections that North Dakota had abandoned. That’s why allowing sales across state lines is even worse for federalism than a needlessly intrusive federal statute. When Congress preempts state law, at least voters in California and New York have a say in the matter. They have no say over North Dakota’s insurance rules.

As it stands, the states already have the authority to permit cross-border sales; indeed, six states have done so.87 And the ACA explicitly authorizes states to band together in “interstate compacts” to enable sales across state lines.88 But it’s one thing for a state to choose to allow its residents to purchase insurance that another state regulates. If Oklahoma has no objection to plans sold by North Dakota insurers, Oklahoma can agree to allow North Dakota plans to be sold in its state. It is another thing altogether to prohibit states from making that choice, as Republican proposals would entail. This is not a strategy to empower the states. It is a strategy to deregulate the insurance market, even in those states that would prefer tighter regulation.

2. Money

Simply wiping the ACA from the books would not enable the states to tackle health reform. Because of the countercyclical trap and ERISA preemption, facilitating a state-centric approach will require Congress to adopt a replacement under which Congress continues to pay for health reform.

Three aspects of Republican proposals—including the AHCA—present cause for concern. First, Congress’s top priority appears to be the adoption of a reconciliation bill that zeroes out the ACA’s taxes.89 The resulting tax break would be enormous: the Congressional Budget Office estimates it will result in a loss to the federal budget of $629.3 billion over ten years.90 Republicans anticipate filling the resulting budget hole by cutting federal spending—including the spending upon which health reform depends.

Second, leading Republican proposals would end the ACA’s rules guaranteeing the affordability of insurance coverage. Under current law, no one making less than four times the poverty level has to devote more than 9.69% of her income toward a typical plan on the ACA’s exchanges (and most pay much less).91 Premium subsidies thus rise and fall with the price of coverage: the cheaper the insurance, the lower the subsidies, and vice versa. Most Republican proposals, however, would key the subsidy to a fixed amount and distribute it based on age, not income.92 Especially for low-income people, those fixed amounts are generally inadequate to adequately defray the cost of coverage, leading to a sharp spike in the rate of the uninsured.93 Worse still, the AHCA does not even index the subsidies to inflation, much less medical inflation, which would lead their value relative to the price of coverage to diminish over time. As coverage becomes more unaffordable, states that wish to maintain universal coverage will have to raise taxes to make up the difference—a difficult trick in light of the countercyclical trap and ERISA preemption.

Third, congressional Republicans hope to transform Medicaid from an individual entitlement to a block grant—a fixed sum of money that places few restrictions on the purposes that states can use it for.94 In some respects, block grant proposals promote federalism: they afford states more discretion about how to put Medicaid dollars to work.95 A state, for example, could place limits on eligibility or benefits; more creatively, it could use some of its Medicaid money for lead abatement in urban cores, as Michigan has recently been allowed to do on a small scale.96 But the devil is in the details. A fixed block grant that increases with economy-wide inflation and is insensitive to the business cycle would not give states the fiscal flexibility necessary to cope with a recession. Over time, as well, the galloping pace of medical inflation would erode the value of the block grants, requiring states to ration access to medical care, either through cuts to benefits or to eligibility.97 Proposals to transform Medicaid into a block-grant program may trade on the rhetoric of states’ rights, but they have the perverse effect of inhibiting state power.

Alternative approaches could mitigate the concern. Per capita grants anchored to a formula that accounted for the number of people within a state under a particular income threshold, for example, would avoid the countercyclical trap: federal outlays would then increase as more people lost their jobs and became dependent on government assistance. But because the data necessary to calculate funding levels may lag the economy by several years, a state could find itself in a financial pinch just as a recession takes hold.98 Nor would a per capita grant account for unanticipated cost spikes associated with the release of costly new therapies (like the new Hepatitis C drugs) or epidemics (like the Zika outbreak). Of greater concern, the size of per capita grants would have to increase with medical inflation.99 Yet Republicans anticipate achieving large cost reductions through Medicaid reform—suggesting that the goal is not to provide sufficient funds to cover those who are currently eligible, but instead to force states to shrink their programs through eligibility restrictions and benefit cuts.100

Conclusion

The first health reform bill introduced in Congress after the 2016 election takes federalism seriously. Supported by a coterie of relatively moderate Republican senators, the Patient Freedom Act of 2017—better-known as Cassidy-Collins for its two principal sponsors—retains the ACA’s taxes and funding streams while giving states a new set of choices about how best to implement reform.101 States can reject the ACA outright, albeit at the cost of federal funding.102 They can adopt an alternative that channels federal money into health savings accounts.103 Or they can stick with the ACA, individual mandate and all.104 In other words, the federal government will pay for reform and the states have a menu of implementation options.105

The prospects for Cassidy-Collins are dim. It lacks support from the Republican leadership, which has so far thrown its weight behind the AHCA. But it offers a model that both parties would do well to examine closely. By giving states more room to chart their own path, the bill embraces the diversity that federalism celebrates. And it does so without cutting states off from the federal financial support that makes health reform possible. The end result will not be pretty: some states will make bad choices about how to reform their health-care systems (although we may disagree about which states those are). But a law along these lines might enable partisans on both sides to move past the rancorous debate over the ACA.106

At a minimum, both Republicans and Democrats should remain attentive to the justifications for vesting the federal government with power over health reform. Neither screeds about federal takeovers nor invectives about the heartlessness of the ACA’s opponents do justice to the complex interplay between state and federal authority. The states can’t act without the federal government: its financial support is the lifeblood of health reform. At the same time, the federal government has little cause to deprive states of the power to decide on the approach to reform that they think best. In a country marked by deep divisions, there is much to be said for an Obamacare replacement that treads as little on state authority as possible.

Nicholas Bagley is a Professor of Law at University of Michigan Law School. I would like to thank Austin Frakt, Mark Hall, Kyle Logue, Adrianna McIntyre, and Gil Seinfeld for their thoughtful comments.

Preferred Citation: Nicholas Bagley, Federalism and the End of Obamacare, 127 Yale L.J. F. 1 (2017), http://www.yalelawjournal.org/forum/federalism-and-the-end-of-obamacare.

Patient Protection and Affordable Care Act, Pub. L. No. 111-148, 124 Stat. 119 (2010) (codified as amended in scattered section of 26 and 42 U.S.C.), amended by Health Care and Education Reconciliation Act of 2010, Pub. L. No. 111-152, 124 Stat. 1029 (2010). For ease of reference, and unless otherwise noted, citations will be to the scattered provisions of the U.S. Code codifying the ACA.

Herbert Wechsler, The Political Safeguards of Federalism: The Role of the States in the Composition and Selection of the National Government, 54 Colum. L. Rev. 543, 544-45 (1954) (“National action has . . . always been regarded as exceptional in our polity, an intrusion to be justified by some necessity, the special rather than the ordinary case . . . . National power may be quite unquestioned in a given situation; those who would advocate its exercise must none the less answer the preliminary question why the matter should not be left to the states.”).

See Julia Zorthian, These Are the States Where SCOTUS Just Legalized Same-Sex Marriage, Time (June 26, 2015), http://time.com/3937662/gay-marriage-supreme-court-states-legal [http://perma.cc/5LKH-3GBG]; see also State-by-State History of Banning and Legalizing Gay Marriage, 1994-2015, ProCon.Org (Feb. 16, 2016), http://gaymarriage.procon.org/view.resource.php?resourceID=004857 [http://perma.cc/7Y5L-KQSX].

Pam Belluck, Massachusetts Set To Offer Universal Health Insurance, N.Y. Times (Apr. 4, 2006), http://www.nytimes.com/2006/04/04/us/04cnd-mass.html [http://perma.cc/2GVB-NKK5].

Paul Ryan, A Better Way: Our Vision for a Confident America 12 (2016), http://www.washingtonpost.com/news/powerpost/wp-content/uploads/sites/47/2016/06/ABetterWay-HealthCare-PolicyPaper.pdf [http://perma.cc/F4QL-NJ9Q].

See Mashaw & Marmor, supra note 9, at 121 n.16 (citing research indicating that “public aid plays a small role in the migration decisions of poor families”). Evidence on migration in response to traditional welfare (e.g., Aid to Families with Dependent Children) is mixed. Even those studies that find a migration effect, however, conclude that it is small. See Jan K. Brueckner, Welfare Reform and Race to the Bottom: Theory and Evidence, 66 Southern Econ. J. 505, 519 (2000).

David K. Ihrke, Carol S. Faber & William K. Koerber, Geographical Mobility: 2008 to 2009, U.S. Census Bureau 16 tbl.7 (2011), http://www.census.gov/prod/2011pubs/p20-565.pdf [http://perma.cc/V4NN-7Q3D] (showing only 2% of people report moving from one county to another for health reasons).

In a pinch, it is possible to tell a story about externalities. The uninsured sometimes go bankrupt on account of their medical bills. When they do, their creditors absorb the loss and serve, in that respect, as insurers of last resort. If most creditors are located out of state, and if those creditors cannot protect themselves in advance by charging higher interest rates to residents of states without near-universal coverage laws, a state’s refusal to expand coverage could allow its residents to impose costs on out-of-state creditors.

These conditions are unlikely to hold to any significant degree, however. Because most health care is locally provided, a bankrupt individual’s medical debt will overwhelmingly be held by local hospitals and care providers. That is not the only debt that matters: bankruptcies arising from medical debt could also harm other non-medical creditors. But mortgage loans constitute the largest source of household debt, and they are linked to in-state property, which allows banks to price the state-specific risk of default into the loans they issue (as well as those they purchase on the secondary market). See N.Y. Fed. Reserve Bank, Quarterly Report on Household Debt and Credit (2016), http://www.newyorkfed.org/medialibrary/interactives/householdcredit/data/pdf/HHDC_2016Q1.pdf [http://perma.cc/BG6V-V8RP]. The same will generally hold for auto loan and credit card debt, even if a small number of consumers will switch states after that debt has been issued. Student loans are trickier: a lender cannot know where a student will move once she finishes her studies, so it cannot price the risk of default arising from unpaid medical bills into her loan. But student loans are almost impossible to discharge in bankruptcy, mitigating the risk considerably. See Bankruptcy Abuse Prevention and Consumer Protection Act of 2005, Pub. L. 109-8, 119 Stat. 23 (2005).

Health Coverage by Race and Ethnicity: The Potential Impact of the Affordable Care Act, Kaiser Family Found. 5 fig.6 (2013), http://kaiserfamilyfoundation.files.wordpress.com/2014/07/8423-health-coverage-by-race-and-ethnicity.pdf [http://perma.cc/JHC8-8Y94].

See John E. McDonough, Inside National Health Reform 41 (2011) (discussing failed reform efforts in Kentucky, Maine, New Hampshire, New Jersey, New York, Vermont, and Washington). The most prominent failure came in 2007, when then-Governor Schwarzenegger of California joined with Democrats in the state legislature to advance an ambitious reform bill, only to watch it crumble. See Marian R. Mulkey & Mark D. Smith, The Long and Winding Road: Reflections On California’s ‘Year Of Health Reform,’ 28 Health Aff. w446 (2009).

For a sampling of the literature on the question, see Peter D. Jacobson, The Role of ERISA Preemption in Health Reform: Opportunities and Limits, 37 J.L. Med. & Ethics 88 (2009); Amy B. Monahan, Pay or Play Laws, ERISA Preemption, and Potential Lessons from Massachusetts, 55 Kan. L. Rev. 1203 (2007); Christen Linke Young, Note, Pay or Play Programs and ERISA Section 514: Proposals for Amending the Statutory Scheme, 10 Yale J. Health Pol’y, L. & Ethics 197 (2010).

See Michael Barbaro, Maryland Sets a Health Cost for Wal-Mart, N.Y. Times (Jan. 13, 2006), http://www.nytimes.com/2006/01/13/business/maryland-sets-a-health-cost-for-walmart.html [http://perma.cc/T7SL-R879].

See Rick Hills, Local Democracy’s Struggle with ERISA Preemption, PrawfsBlawg (Dec. 26, 2008, 10:29 AM), http://prawfsblawg.blogs.com/prawfsblawg/2008/12/city-power-to-impose-healthcare-mandates-on-employers-erisa.html [http://perma.cc/PQ3U-QVGH]; Roderick M. Hills, Jr., Against Preemption: How Federalism Can Improve the Federal Legislative Process, 82 N.Y.U. L. Rev. 1 (2007).

See 42 U.S.C. § 18022 (2012). By regulation, HHS asked the states to designate a “benchmark plan” from a list of plans in which their residents are already enrolled. Whatever benefits are covered by the benchmark plans would then be considered essential. See Nicholas Bagley & Helen Levy, Essential Health Benefits and the Affordable Care Act, 39 J. Health Pol., Pol’y & L. 441 (2014).

Ctrs. for Medicare & Medicaid Servs., Fact Sheet: Hawai’i: State Innovation Waiver (2016), http://www.cms.gov/CCIIO/Programs-and-Initiatives/State-Innovation-Waivers/Downloads/Hawaii-1332-Waiver-Fact-Sheet-12-30-16-FINAL.pdf [http://perma.cc/JRT4-94AQ].

See Philip Klein, GOP Will Fail on Obamacare If They Can’t Admit a Simple Truth, Wash. Examiner (Jan. 6, 2017), http://www.washingtonexaminer.com/gop-will-fail-on-obamacare-if-they-cant-admit-a-simple-truth/article/2611075 [http://perma.cc/2HZA-ATTD].

See Paul Starr, The Mandate Miscalculation, New Republic (Dec. 14, 2011), http://newrepublic.com/article/98554/individual-mandate-affordable-care-act. [http://perma.cc/3VE7-E5HK].

David Super has argued that programs based on unrestricted grants—money with few or no strings—have proven fragile because “federal policymakers . . . must bear the political costs of raising the revenue and forgo the political rewards of spending that revenue on programs for which they would receive political credit.” Super, supra note 10, at 2557-58 n.54; see also Super, supra note 73, at 710-11. Super’s point is well-taken, but adding strings to federal money can create its own form of fragility: states may bridle so much at the restrictions that they agitate for radically altering or undoing the program altogether. In the politically contentious environment of health reform, relaxing federal control may enhance sustainability, even if federal policymakers can claim somewhat less credit for reform than they might have if they had imposed more restrictions on federal funds.

See Gluck, supra note 11, at 1751; see also Abbe R. Gluck, Our [National] Federalism, 123 Yale L.J. 1996, 1997 (2014) (“With almost every national statutory step, Congress gives states new governing opportunities or incorporates aspects of state law—displacing state authority with one hand and giving it back with the other.”).

See Yuval Levin, The Waivers Question, Nat’l Review (Apr. 5, 2017, 9:48 AM), http://www.nationalreview.com/corner/446453/gop-health-debate-continues-yuval-levin [http://perma.cc/ZC6C-MTB7].

In particular, the American Health Care Act (AHCA) offers the most detailed insight into Republican priorities. See 115th Cong., Budget Reconciliation Legislative Recommendations Relating to Repeal and Replace of the Patient Protection and Affordable Care Act (Comm. Print 2017), http://energycommerce.house.gov/sites/republicans.energycommerce.house.gov/files/documents/AmericanHealthCareAct.pdf [http://perma.cc/3QC9-MKY3].

See Caitlin Owens, Why Trumpcare Might Sign You Up For Health Insurance Without Asking, Axios (Jan. 19, 2017), http://www.axios.com/why-trumpcare-might-sign-you-up-for-health-insurance-without-asking-2162181493.html [http://perma.cc/3D93-VCEP].

See Nicholas Bagley, Patching Obamacare at the State Level, Incidental Economist (Dec. 16, 2016, 7:41 AM), http://theincidentaleconomist.com/patching-obamacare-at-the-state-level [http://perma.cc/SU7D-6R9V].

See Michael Ollove, Interstate Health Insurance: Sounds Good, But Details Are Tricky, Pew Charitable Trusts: Stateline (Jan. 18, 2017), http://www.pewtrusts.org/en/research-and-analysis/blogs/stateline/2017/01/18/interstate-health-insurance-sounds-good-but-details-are-tricky [http://perma.cc/XV57-7R2Q].

See Sabrina Corlette et al., Selling Health Insurance Across State Lines: An Assessment of State Laws and Implications for Improving Choice and Affordability of Coverage, Ctr. on Health Ins. Reforms 6 (Oct. 2012), http://www.rwjf.org/content/dam/farm/reports/issue_briefs/2012/rwjf401409 [http://perma.cc/3LVJ-ZV2N].

See Sarah Kliff, Senate Republicans Just Introduced an Obamacare Repeal Plan Democrats Can’t Stop, Vox (Jan. 3, 2017, 2:10 PM), http://www.vox.com/policy-and-politics/2017/1/3/14154820/senate-obamacare-budget-resolution-reconciliation [http://perma.cc/93ZR-X36A].

Letter from Keith Hall, Dir., Cong. Budget Office, to Senator Mike Enzi, Chairman, Comm. on the Budget 6-7 (Dec. 11, 2015), http://www.cbo.gov/sites/default/files/114th-congress-2015-2016/costestimate/hr3762senatepassed.pdf [http://perma.cc/J9W9-T5MZ].

Staff of H. Comm. on Ways & Means, 115th Cong., Budget Reconciliation Legislative Recommendations Relating to Remuneration from Certain Insurers § __15, at 19 (Comm. Print 2017), http://waysandmeans.house.gov/wp-content/uploads/2017/03/AmericanHealthCareAct_WM.pdf [http://perma.cc/B3C3-ZV5N] (adding section 36C to the Internal Revenue Code).

See Joseph Antos & James Capretta, The House Republicans’ Health Plan, Health Affairs Blog (June 22, 2016), http://healthaffairs.org/blog/2016/06/22/the-house-republicans-health-plan [http://perma.cc/C62E-PC3L].

Press Release, Centers for Medicare & Medicaid Services, CMS Approves Michigan Plan To Abate Lead Hazards From Flint And Other Impacted Areas In The State With Federal Support (Nov. 14, 2016), http://www.cms.gov/Newsroom/MediaReleaseDatabase/Fact-sheets/2016-Fact-sheets-items/2016-11-14-3.html [http://perma.cc/AKS9-TNTN].

Andrew J. Goodman-Bacon & Sayeh S. Nikpay, Per Capita Caps in Medicaid—Lessons from the Past, 376 New Eng. J. Med. 1005, 1005 (2017) (arguing that historical experience suggests that “Ryan’s proposal would result in restrictions on coverage and benefits rather than state innovations to reduce program costs”).

See Edwin Park, Like a Block Grant, Medicaid Per Capita Cap Would Shift Costs to States and Place Beneficiaries at Risk, Ctr. Budget & Pol’y Priorities (June 16, 2016), http://www.cbpp.org/sites/default/files/atoms/files/6-16-16health-commentary.pdf [http://perma.cc/339U-KAVU].