Amazon’s Antitrust Paradox

abstract. Amazon is the titan of twenty-first century commerce. In addition to being a retailer, it is now a marketing platform, a delivery and logistics network, a payment service, a credit lender, an auction house, a major book publisher, a producer of television and films, a fashion designer, a hardware manufacturer, and a leading host of cloud server space. Although Amazon has clocked staggering growth, it generates meager profits, choosing to price below-cost and expand widely instead. Through this strategy, the company has positioned itself at the center of e-commerce and now serves as essential infrastructure for a host of other businesses that depend upon it. Elements of the firm’s structure and conduct pose anticompetitive concerns—yet it has escaped antitrust scrutiny.

This Note argues that the current framework in antitrust—specifically its pegging competition to “consumer welfare,” defined as short-term price effects—is unequipped to capture the architecture of market power in the modern economy. We cannot cognize the potential harms to competition posed by Amazon’s dominance if we measure competition primarily through price and output. Specifically, current doctrine underappreciates the risk of predatory pricing and how integration across distinct business lines may prove anticompetitive. These concerns are heightened in the context of online platforms for two reasons. First, the economics of platform markets create incentives for a company to pursue growth over profits, a strategy that investors have rewarded. Under these conditions, predatory pricing becomes highly rational—even as existing doctrine treats it as irrational and therefore implausible. Second, because online platforms serve as critical intermediaries, integrating across business lines positions these platforms to control the essential infrastructure on which their rivals depend. This dual role also enables a platform to exploit information collected on companies using its services to undermine them as competitors.

This Note maps out facets of Amazon’s dominance. Doing so enables us to make sense of its business strategy, illuminates anticompetitive aspects of Amazon’s structure and conduct, and underscores deficiencies in current doctrine. The Note closes by considering two potential regimes for addressing Amazon’s power: restoring traditional antitrust and competition policy principles or applying common carrier obligations and duties.

author. I am deeply grateful to David Singh Grewal for encouraging me to pursue this project and to Barry C. Lynn for introducing me to these issues in the first place. For thoughtful feedback at various stages of this project, I am also grateful to Christopher R. Leslie, Daniel Markovits, Stacy Mitchell, Frank Pasquale, George Priest, Maurice Stucke, and Sandeep Vaheesan. Lastly, many thanks to Juliana Brint, Urja Mittal, and the Yale Law Journal staff for insightful comments and careful editing. All errors are my own.

Introduction

“Even as Amazon became one of the largest retailers in the country, it never seemed interested in charging enough to make a profit. Customers celebrated and the competition languished.”

—The New York Times1

“[O]ne of Mr. Rockefeller’s most impressive characteristics is patience.”

—Ida Tarbell, A History of the Standard Oil Company2

In Amazon’s early years, a running joke among Wall Street analysts was that CEO Jeff Bezos was building a house of cards. Entering its sixth year in 2000, the company had yet to crack a profit and was mounting millions of dollars in continuous losses, each quarter’s larger than the last. Nevertheless, a segment of shareholders believed that by dumping money into advertising and steep discounts, Amazon was making a sound investment that would yield returns once e-commerce took off. Each quarter the company would report losses, and its stock price would rise. One news site captured the split sentiment by asking, “Amazon: Ponzi Scheme or Wal-Mart of the Web?”3

Sixteen years on, nobody seriously doubts that Amazon is anything but the titan of twenty-firstcentury commerce. In 2015, it earned $107 billion in revenue,4 and, as of 2013, it sold more than its next twelve online competitors combined.5 By some estimates, Amazon now captures 46% of online shopping, with its share growing faster than the sector as a whole.6 In addition to being a retailer, it is a marketing platform, a delivery and logistics network, a payment service, a credit lender, an auction house, a major book publisher, a producer of television and films, a fashion designer, a hardware manufacturer, and a leading provider of cloud server space and computing power. Although Amazon has clocked staggering growth—reporting double-digit increases in net sales yearly—it reports meager profits, choosing to invest aggressively instead. The company listed consistent losses for the first seven years it was in business, with debts of $2 billion.7 While it exits the red more regularly now,8 negative returns are still common. The company reported losses in two of the last five years, for example, and its highest yearly net income was still less than 1% of its net sales.9

Despite the company’s history of thin returns, investors have zealously backed it: Amazon’s shares trade at over 900 times diluted earnings, making it the most expensive stock in the Standard & Poor’s 500.10 As one reporter marveled, “The company barely ekes out a profit, spends a fortune on expansion and free shipping and is famously opaque about its business operations. Yet investors . . . pour into the stock.”11 Another commented that Amazon is in “a class of its own when it comes to valuation.”12

Reporters and financial analysts continue to speculate about when and how Amazon’s deep investments and steep losses will pay off.13 Customers, meanwhile, universally seem to love the company. Close to half of all online buyers go directly to Amazon first to search for products,14 and in 2016, the Reputation Institute named the firm the “most reputable company in America” for the third year running.15 In recent years, journalists have exposed the aggressive business tactics Amazon employs. For instance Amazon named one campaign “The Gazelle Project,” a strategy whereby Amazon would approach small publishers “the way a cheetah would a sickly gazelle.”16 This, as well as other reporting,17 drew widespread attention,18 perhaps because it offered a glimpse at the potential social costs of Amazon’s dominance. The firm’s highly public dispute with Hachette in 2014—in which Amazon delisted the publisher’s books from its website during business negotiations—similarly generated extensive press scrutiny and dialogue.19 More generally, there is growing public awareness that Amazon has established itself as an essential part of the internet economy,20 and a gnawing sense that its dominance—its sheer scale and breadth—may pose hazards.21 But when pressed on why, critics often fumble to explain how a company that has so clearly delivered enormous benefits to consumers—not to mention revolutionized e-commerce in general—could, at the end of the day, threaten our markets. Trying to make sense of the contradiction, one journalist noted that the critics’ argument seems to be that “even though Amazon’s activities tend to reduce book prices, which is considered good for consumers, they ultimately hurt consumers.”22

In some ways, the story of Amazon’s sustained and growing dominance is also the story of changes in our antitrust laws. Due to a change in legal thinking and practice in the 1970s and 1980s, antitrust law now assesses competition largely with an eye to the short-term interests of consumers, not producers or the health of the market as a whole; antitrust doctrine views low consumer prices, alone, to be evidence of sound competition. By this measure, Amazon has excelled; it has evaded government scrutiny in part through fervently devoting its business strategy and rhetoric to reducing prices for consumers. Amazon’s closest encounter with antitrust authorities was when the Justice Department sued other companies for teaming up against Amazon.23 It is as if Bezos charted the company’s growth by first drawing a map of antitrust laws, and then devising routes to smoothly bypass them. With its missionary zeal for consumers, Amazon has marched toward monopoly by singing the tune of contemporary antitrust.

This Note maps out facets of Amazon’s power. In particular, it traces the sources of Amazon’s growth and analyzes the potential effects of its dominance. Doing so enables us to make sense of the company’s business strategy and illuminates anticompetitive aspects of its structure and conduct. This analysis reveals that the current framework in antitrust—specifically its equating competition with “consumer welfare,” typically measured through short-term effects on price and output24—fails to capture the architecture of market power in the twenty-first century marketplace. In other words, the potential harms to competition posed by Amazon’s dominance are not cognizable if we assess competition primarily through price and output. Focusing on these metrics instead blinds us to the potential hazards.

My argument is that gauging real competition in the twenty-first century marketplace—especially in the case of online platforms—requires analyzing the underlying structure and dynamics of markets. Rather than pegging competition to a narrow set of outcomes, this approach would examine the competitive process itself. Animating this framework is the idea that a company’s power and the potential anticompetitive nature of that power cannot be fully understood without looking to the structure of a business and the structural role it plays in markets. Applying this idea involves, for example, assessing whether a company’s structure creates certain anticompetitive conflicts of interest; whether it can cross-leverage market advantages across distinct lines of business; and whether the structure of the market incentivizes and permits predatory conduct.

This is the approach I adopt in this Note. I begin by exploring—and challenging—modern antitrust law’s treatment of market structure. Part I gives an overview of the shift in antitrust away from economic structuralism in favor of price theory and identifies how this departure has played out in two areas of enforcement: predatory pricing and vertical integration. Part II questions this narrow focus on consumer welfare as largely measured by prices, arguing that assessing structure is vital to protect important antitrust values. The Note then uses the lens of market structure to reveal anticompetitive aspects of Amazon’s strategy and conduct. Part III documents Amazon’s history of aggressive investing and loss leading, its company strategy, and its integration across many lines of business. Part IV identifies two instances in which Amazon has built elements of its business through sustained losses, crippling its rivals, and two instances in which Amazon’s activity across multiple business lines poses anticompetitive threats in ways that the current framework fails to register. The Note then assesses how antitrust law can address the challenges raised by online platforms like Amazon. Part V considers what capital markets suggest about the economics of Amazon and other internet platforms. Part VI offers two approaches for addressing the power of dominant platforms: (1) limiting their dominance through restoring traditional antitrust and competition policy principles and (2) regulating their dominance by applying common carrier obligations and duties.

I. the chicago school revolution: the shift away from competitive process and market structure

One of the most significant changes in antitrust law and interpretation over the last century has been the move away from economic structuralism. In this Part, I trace this history by sketching out how a structure-based view of competition has been replaced by price theory and exploring how this shift has played out through changes in doctrine and enforcement.

Broadly, economic structuralism rests on the idea that concentrated market structures promote anticompetitive forms of conduct.25 This view holds that a market dominated by a very small number of large companies is likely to be less competitive than a market populated with many small- and medium-sized companies. This is because: (1) monopolistic and oligopolistic market structures enable dominant actors to coordinate with greater ease and subtlety, facilitating conduct like price-fixing, market division, and tacit collusion; (2) monopolistic and oligopolistic firms can use their existing dominance to block new entrants; and (3) monopolistic and oligopolistic firms have greater bargaining power against consumers, suppliers, and workers, which enables them to hike prices and degrade service and quality while maintaining profits.

This market structure-based understanding of competition was a foundation of antitrust thought and policy through the 1960s. Subscribing to this view, courts blocked mergers that they determined would lead to anticompetitive market structures. In some instances, this meant halting horizontal deals—mergers combining two direct competitors operating in the same market or product line—that would have handed the new entity a large share of the market.26 In others, it involved rejecting vertical mergers—deals joining companies that operated in different tiers of the same supply or production chain—that would “foreclose competition.”27 Centrally, this approach involved policing not just for size but also for conflicts of interest—like whether allowing a dominant shoe manufacturer to extend into shoe retailing would create an incentive for the manufacturer to disadvantage or discriminate against competing retailers.28

The Chicago School approach to antitrust, which gained mainstream prominence and credibility in the 1970s and 1980s, rejected this structuralist view.29 In the words of Richard Posner, the essence of the Chicago School position is that “the proper lens for viewing antitrust problems is price theory.”30 Foundational to this view is a faith in the efficiency of markets, propelled by profit-maximizing actors. The Chicago School approach bases its vision of industrial organization on a simple theoretical premise: “[R]ational economic actors working within the confines of the market seek to maximize profits by combining inputs in the most efficient manner. A failure to act in this fashion will be punished by the competitive forces of the market.”31

While economic structuralists believe that industrial structure predisposes firms toward certain forms of behavior that then steer market outcomes, the Chicago School presumes that market outcomes—including firm size, industry structure, and concentration levels—reflect the interplay of standalone market forces and the technical demands of production.32 In other words, economic structuralists take industry structure as an entryway for understanding market dynamics, while the Chicago School holds that industry structure merely reflects such dynamics. For the Chicago School, “[w]hat exists is ultimately the best guide to what should exist.”33

Practically, the shift from structuralism to price theory had two major ramifications for antitrust analysis. First, it led to a significant narrowing of the concept of entry barriers. An entry barrier is a cost that must be borne by a firm seeking to enter an industry but is not carried by firms already in the industry.34 According to the Chicago School, advantages that incumbents enjoy from economies of scale, capital requirements, and product differentiation do not constitute entry barriers, as these factors are considered to reflect no more than the “objective technical demands of production and distribution.”35 With so many “entry barriers . . . discounted, all firms are subject to the threat of potential competition . . . regardless of the number of firms or levels of concentration.”36 On this view, market power is always fleeting—and hence antitrust enforcement rarely needed.

The second consequence of the shift away from structuralism was that consumer prices became the dominant metric for assessing competition. In his highly influential work, The Antitrust Paradox, Robert Bork asserted that the sole normative objective of antitrust should be to maximize consumer welfare, best pursued through promoting economic efficiency.37 Although Bork used “consumer welfare” to mean “allocative efficiency,”38 courts and antitrust authorities have largely measured it through effects on consumer prices. In 1979, the Supreme Court followed Bork’s work and declared that “Congress designed the Sherman Act as a ‘consumer welfare prescription’”39—a statement that is widely viewed as erroneous.40 Still, this philosophy wound its way into policy and doctrine. The 1982 merger guidelines issued by the Reagan Administration—a radical departure from the previous guidelines, written in 1968—reflected this newfound focus. While the 1968 guidelines had established that the “primary role” of merger enforcement was “to preserve and promote market structures conducive to competition,”41 the 1982 guidelines said mergers “should not be permitted to create or enhance ‘market power,’” defined as the “ability of one or more firms profitably to maintain prices above competitive levels.”42 Today, showing antitrust injury requires showing harm to consumer welfare, generally in the form of price increases and output restrictions.43

It is true that antitrust authorities do not ignore non-price effects entirely. The 2010 Horizontal Merger Guidelines, for example, acknowledge that enhanced market power can manifest as non-price harms, including in the form of reduced product quality, reduced product variety, reduced service, or diminished innovation.44 Notably, the Obama Administration’s opposition to one of the largest mergers proposed on its watch—Comcast/TimeWarner—stemmed from a concern about market access, not prices.45 And by some measures, the Federal Trade Commission (FTC) has alleged potential harm to innovation in roughly one-third of merger enforcement actions in the last decade.46 Still, it is fair to say that a concern for innovation or non-price effects rarely animates or drives investigations or enforcement actions—especially outside of the merger context.47 Economic factors that are easier to measure—such as impacts on price, output, or productive efficiency in narrowly defined markets—have become “disproportionately important.”48

Two areas of enforcement that this reorientation has affected dramatically are predatory pricing and vertical integration. The Chicago School claims that “predatory pricing, vertical integration, and tying arrangements never or almost never reduce consumer welfare.”49 Both predatory pricing and vertical integration are highly relevant to analyzing Amazon’s path to dominance and the source of its power. Below, I offer a brief overview of how the Chicago School’s influence has shaped predatory pricing doctrine and enforcers’ views of vertical integration.

A. Predatory Pricing

Through the mid-twentieth century, Congress repeatedly enacted legislation targeting predatory pricing. Congress, as well as state legislatures, viewed predatory pricing as a tactic used by highly capitalized firms to bankrupt rivals and destroy competition—in other words, as a tool to concentrate control. Laws prohibiting predatory pricing were part of a larger arrangement of pricing laws that sought to distribute power and opportunity. However, a controversial Supreme Court decision in the 1960s created an opening for critics to attack the regime. This intellectual backlash wound its way into Supreme Court doctrine by the early 1990s in the form of the restrictive “recoupment test.”

The earliest predatory pricing case in America was the government’s antitrust suit against Standard Oil, which reached the Supreme Court in 1911.50 As detailed in Ida Tarbell’s exposé, A History of the Standard Oil Company, Standard Oil routinely slashed prices in order to drive rivals from the market.51 Moreover, it cross-subsidized: Standard Oil charged monopoly prices52 in markets where it faced no competitors; in markets where rivals checked the company’s dominance, it drastically lowered prices in an effort to push them out. In its antitrust case against the company, the government argued that a suite of practices by Standard Oil—including predatory pricing—violated section 2 of the Sherman Act. The Supreme Court ruled for the government and ordered the break-up of the company.53 Subsequent courts cited the decision for establishing that in the quest for monopoly power, “price cutting became perhaps the most effective weapon of the larger corporation.”54

Recognizing the threat of predatory pricing executed by Standard Oil, Congress passed a series of laws prohibiting such conduct. In 1914 Congress enacted the Clayton Act55 to strengthen the Sherman Act and included a provision to curb price discrimination and predatory pricing.56 The House Report stated that section 2 of the Clayton Act was expressly designed to prohibit large corporations from slashing prices below the cost of production “with the intent to destroy and make unprofitable the business of their competitors” and with the aim of “acquiring a monopoly in the particular locality or section in which the discriminating price is made.”57

Congress also acted to protect state “fair trade” laws that further safeguarded against predatory pricing. Fair trade legislation granted producers the right to set the final retail price of their goods, limiting the ability of chain stores to discount.58 When the Supreme Court targeted these “resale price maintenance” efforts, Congress stepped up to defend them. After the Supreme Court in 1911 struck down the form of resale price maintenance enabled by fair trade laws,59 Congress in 1937 carved out an exception for state fair trade laws through the Miller-Tydings Act.60 When the Supreme Court in 1951 ruled that producers could enforce minimum prices only against those retailers that had signed contracts agreeing to do so,61 Congress responded with a law making minimum prices enforceable against nonsigners too.62

Another byproduct of the “fair trade” movement was the Robinson-Patman Act of 1936. This Act prohibited price discrimination by retailers among producers and by producers among retailers.63 Its aim was to prevent conglomerates and large companies from using their buyer power to extract crippling discounts from smaller entities, and to keep large manufacturers and retailers from teaming up against rivals.64 Like laws banning predatory pricing, the prohibition against price discrimination effectively curbed the power of size. Section 3 of the Act addressed predatory pricing directly by making it a crime to sell goods at “unreasonably low prices for the purpose of destroying competition or eliminating a competitor.”65 While predatory price cutting gave rise to civil liability and remedies under the Clayton Act, the Robinson-Patman Act attached criminal penalties as well.66

This series of antitrust laws demonstrates that Congress saw predatory pricing as a serious threat to competitive markets. By the mid-twentieth century, the Supreme Court recognized and gave effect to this congressional intent. The Court upheld the Robinson-Patman Act numerous times, holding that the relevant factors were whether a retailer intended to destroy competition through its pricing practices and whether its conduct furthered that purpose.67 However, not all instances of below-cost pricing were illegitimate. Liquidating excess or perishable goods, for example, was considered fair game.68 Only “sales made below cost without legitimate commercial objective and with specific intent to destroy competition” would clearly violate section 3.69 In other cases, the Court distinguished between competitive advantages drawn from superior skill and production, and those drawn from the brute power of size and capital.70 The latter, the Court ruled, were illegitimate.71

In Utah Pie Co. v. Continental Baking Co.,the Court further reinforced the illegitimacy of predatory pricing.72 Utah Pie and Continental Baking were competing manufacturers of frozen dessert pies. A locational advantage gave Utah Pie cheaper access to the Salt Lake City market, which it used to price goods below those sold by competitors. Other frozen pie manufacturers, including Continental, began selling at below-cost prices in the Salt Lake City market, while keeping prices in other regions at or above cost. Utah Pie brought a predatory pricing case against Continental. The Supreme Court ruled for Utah Pie, noting that the pricing strategies of its competitors had diverted business from Utah Pie and compelled the company to further lower its prices, leading to a “declining price structure” overall.73 Additionally, Continental had admitted to sending an industrial spy to Utah Pie’s plant to gain information to sabotage Utah’s business relations with retailers, a fact the Court used to establish “intent to injure.”74

The decision was controversial. Continental’s conduct had loosened the grip of a quasi-monopolist. Prior to the alleged predation, Utah Pie had controlled 66.5% of the Salt Lake City market, but following Continental’s practices, its share dropped to 45.3%.75 Penalizing conduct that had made a market more competitive as predatory seemed perverse. As Justice Stewart noted in the dissent, “I cannot hold that Utah Pie’s monopolistic position was protected by the federal antitrust laws from effective price competition . . . .”76

The case presented an opportunity for critics of predatory pricing laws to attack the doctrine as misguided. In an article labeling Utah Pie “the most anticompetitive antitrust decision of the decade,” Ward Bowman, an economist at Yale Law School, argued that the premise of predatory pricing laws was wrong.77 He wrote, “The Robinson-Patman Act rests upon a presumption that price discrimination can or might be used as a monopolizing technique. This, as more recent economic literature confirms, is at best a highly dubious presumption.”78 Bork, meanwhile, said of the decision, “There is no economic theory worthy of the name that could find an injury to competition on the facts of the case. Defendants were convicted not of injuring competition but, quite simply, of competing.”79 He described predatory pricing generally as “a phenomenon that probably does not exist” and the Robinson-Patman Act as “the misshapen progeny of intolerable draftsmanship coupled to wholly mistaken economic theory.”80 Other scholars, particularly those from the rising Chicago School, also weighed in to criticize Utah Pie.81

As the writings of Bowman and Bork suggest, the Chicago School critique of predatory pricing doctrine rests on the idea that below-cost pricing is irrational and hence rarely occurs.82 For one, the critics argue, there was no guarantee that reducing prices below cost would either drive a competitor out or otherwise induce the rival to stop competing. Second, even if a competitor were to drop out, the predator would need to sustain monopoly pricing for long enough to recoup the initial losses and successfully thwart entry by potential competitors, who would be lured by the monopoly pricing. The uncertainty of its success, coupled with its guarantee of costs, made predatory pricing an unappealing—and therefore highly unlikely—strategy.83

As the influence and credibility of these scholars grew, their thinking shaped government enforcement. During the 1970s, for example, the number of Robinson-Patman Act cases that the FTC brought dropped dramatically, reflecting the belief that these cases were of little economic concern.84 Under the Reagan Administration, the FTC all but entirely abandoned Robinson-Patman Act cases.85 Bork’s appointment as Solicitor General, meanwhile, gave him a prime platform to influence the Supreme Court on antitrust issues and enabled him “to train and influence many of the attorneys who would argue before the Supreme Court for the next generation.”86

The Chicago School critique came to shape Supreme Court doctrine on predatory pricing. The depth and degree of this influence became apparent in Matsushita Electric Industrial Co. v. Zenith Radio Corp.87 Zenith, an American manufacturer of consumer electronics, brought a Sherman Act section 1 case accusing Japanese firms of conspiring to charge predatorily low prices in the U.S. market in order to drive American companies out of business.88 The Supreme Court granted certiorari to review whether the Third Circuit had applied the correct standard in reversing the district court’s grant of summary judgment to Matsushita—an inquiry that led the Court to assess the reasonableness of assuming the alleged predation.89

Citing to Bork’s The Antitrust Paradox, the Court concluded that predatory pricing schemes were implausible and therefore could not justify a reasonable assumption in favor of Zenith. “As [Bork’s work] shows, the success of such schemes is inherently uncertain: the short-run loss is definite, but the long-run gain depends on successfully neutralizing the competition,” the Court wrote.90 “For this reason, there is a consensus among commentators that predatory pricing schemes are rarely tried, and even more rarely successful.”91

In addition to adopting Bork’s cost-benefit framing, the Court echoed his concern that price competition could be mistaken for predation. In The Antitrust Paradox,Bork wrote, “The real danger for the law is less that predation will be missed than that normal competitive behavior will be wrongly classified as predatory and suppressed.”92 Justice Powell, writing for the 5-4 majority in Matsushita, echoed Bork: “[C]utting prices in order to increase business often is the very essence of competition. Thus mistaken inferences in cases such as this one are especially costly, because they chill the very conduct the antitrust laws are designed to protect.”93

Although Matsushita focused on a narrow issue—the summary judgment standard for claims brought under Section 1 of the Sherman Act, which targets coordinationamong parties94—it has been widely influential in monopolization cases, which fall under Section 2. In other words, reasoning that originated in one context has wound up in jurisprudence applying to totally distinct circumstances, even as the underlying violations differ vastly.95 Subsequent courts applied Matsushita’s predatory pricing analysis to cases involving monopolization and unilateral anticompetitive conduct, shaping the jurisprudence of Section 2 of the Sherman Act.96 The lower courts seized on Matsushita’s central point: the idea that “predatory pricing schemes are rarely tried, and even more rarely successful.”97 The phrase became a talisman against the existence of predatory pricing, routinely invoked by courts in favor of defendants.

In Brooke Group Ltd. v. Brown & Williamson Tobacco Corp.,98 the Supreme Court formalized this premise into a doctrinal test.The case involved cigarette manufacturing, an industry dominated by six firms.99 Liggett, one of the six, introduced a line of generic cigarettes, which it sold for about 30% less than the price of branded cigarettes.100 Liggett alleged that when it became clear that its generics were diverting business from branded cigarettes, Brown & Williamson, a competing manufacturer, began selling its own generics at a loss.101 Liggett sued, claiming that Brown & Williamson’s tactic was designed to pressure Liggett to raise prices on its generics, thus enabling Brown & Williamson to maintain high profits on branded cigarettes. A jury returned a verdict in favor of Liggett, but the district court judge decided that Brown & Williamson was entitled to judgment as a matter of law.102

Importantly, Liggett’s accusation was that Brown & Williamson would recoup its losses through raising prices on branded cigarettes, not the generics cigarettes it was steeply discounting. Building on the analysis introduced in Matsushita, the Court held that Liggett had failed to show that Brown & Williamson would be able to execute the scheme successfully by recouping its losses through supracompetitive pricing. “Evidence of below-cost pricing is not alone sufficient to permit an inference of probable recoupment and injury to competition,” Justice Kennedy wrote for the majority.103 Instead, the plaintiff “must demonstrate that there is a likelihood that the predatory scheme alleged would cause a rise in prices above a competitive level that would be sufficient to compensate for the amounts expended on the predation, including the time value of the money invested in it”104—a requirement now known as the “recoupment test.”

In placing recoupment at the center of predatory pricing analysis, the Court presumed that direct profit maximization is the singular goal of predatory pricing.105 Furthermore, by establishing that harm occurs only when predatory pricing results in higher prices, the Court collapsed the rich set of concerns that had animated earlier critics of predation, including an aversion to large firms that exploit their size and a desire to preserve local control. Instead, the Court adopted the Chicago School’s narrow conception of what constitutes this harm (higher prices) and how this harm comes about—namely, through the alleged predator raising prices on the previously discounted good.106

Today, succeeding on a predatory pricing claim requires a plaintiff to meet the Brooke Group recoupment test by showing that the defendant would be able to recoup its losses through sustaining supracompetitive prices. Since the Court introduced this recoupment requirement, the number of cases brought and won by plaintiffs has dropped dramatically.107 Despite the Court’s contention—that “predatory pricing schemes are rarely tried and even more rarely successful”—a host of research shows that predatory pricing can be “an attractive anticompetitive strategy” and has been used by dominant firms across sectors to squash or deter competition.108

B. Vertical Integration

Analysis of vertical integration has similarly moved away from structural concerns. Vertical integration arises when “two or more successive stages of production and/or distribution of a product are combined under the same control.”109 For most of the last century, enforcers reviewed vertical integration under the same standards as horizontal mergers, as set out in the Sherman Act, the Clayton Act, and the Federal Trade Commission Act. Vertical integration was banned whenever it threatened to “substantially lessen competition”110 or constituted a “restraint of trade”111 or an “unfair method[] of competition.”112 However, the Chicago School’s view that vertical mergers are generally pro-competitive has led enforcement in this area to significantly drop.

Serious concern about vertical integration took hold in the wake of the Great Depression, when both the law and economic theory became sharply critical of the phenomenon.113 Thurman Arnold, the Assistant Attorney General in the 1930s, targeted vertical ownership achieved through both mergers and contractual provisions, and by the 1950s courts and antitrust authorities generally viewed vertical integration as anticompetitive. Partly because it believed that the Supreme Court had failed to use existing law to block vertical integration through acquisitions, Congress in 1950 amended section 7 of the Clayton Act to make it applicable to vertical mergers.114

Critics of vertical integration primarily focused on two theories of potential harm: leverage and foreclosure. Leverage reflects the idea that a firm can use its dominance in one line of business to establish dominance in another. Because “horizontal power in one market or stage of production creates ‘leverage’ for the extension of the power to bar entry at another level,” vertical integration combined with horizontal market power “can impair competition to a greater extent than could the exercise of horizontal power alone.”115 Foreclosure, meanwhile, occurs when a firm uses one line of business to disadvantage rivals in another line. A flourmill that also owned a bakery could hike prices or degrade quality when selling to rival bakers—or refuse to do business with them entirely. In this view, even if an integrated firm did not directly resort to exclusionary tactics, the arrangement would still increase barriers to entry by requiring would-be entrants to compete at two levels.

When seeking to block vertical combinations or arrangements, the government frequently built its case on one of these theories—and, through the 1960s, courts largely accepted them.116 In Brown Shoe v. United States, for example, the government sought to block a merger between a leading manufacturer and a leading retailer of shoes on the grounds that the tie-up would “foreclos[e] competition” and “enhanc[e] Brown’s competitive advantage over other producers, distributors and sellers of shoes.”117 The Court acknowledged that the Clayton Act did not “render unlawful all . . . vertical arrangements,” but held that this merger would undermine competition by “foreclos[ing] . . . independent manufacturers from markets otherwise open to them.”118 In other words, the concern was that—once merged—the combined entity would forbid its retailing arm from stocking shoes made by competing independent manufacturers. Calling this form of foreclosure “the primary vice of a vertical merger,”119 the Court noted it was also largely inevitable: “Every extended vertical arrangement by its very nature, for at least a time, denies to competitors of the supplier the opportunity to compete for part or all of the trade of the customer-party to the vertical arrangement.”120 In his partial concurrence, Justice Harlan observed that the deal would enable Brown to “turn an independent purchaser into a captive market for its shoes,” thereby “diminish[ing] the available market for which shoe manufacturers compete.”121 The Court enjoined the merger.122

Another reason courts cited for blocking these arrangements was that vertical deals eliminated potential rivals—a recognition of how a merger would reshape industry structure. Upholding the FTC’s challenge of Ford purchasing an equipment manufacturer, the Court noted that before the acquisition, Ford had helped check the power of the manufacturers and had a “soothing influence” over prices.123 An outside firm “may someday go in and set the stage for noticeable deconcentration,” the Court wrote.124 “While it merely stays near the edge, it is a deterrent to current competitors.”125 In other words, the threat of potential entry by Ford—the fact that, pre-merger, it could have internally expanded into equipment manufacturing—had played an important disciplining role. Relatedly, the Court observed that when a company in a competitive market integrates with a firm in an oligopolistic one, the merger can have “the result of transmitting the rigidity of the oligopolistic structure” of one industry to the other, “thus reducing the chances of future deconcentration” of the market.126 The Court required Ford to divest the manufacturer.127

In the 1950s—while Congress, enforcement agencies, and the courts recognized potential threats posed by vertical arrangements—Chicago School scholars began to cast doubt on the idea that vertical integration has anticompetitive effects.128 By replacing market transactions with administrative decisions within the firm, they argued, vertical arrangements generated efficiencies that antitrust law should promote. And if integration failed to yield efficiencies, then the integrated firm would have no cost advantages over unintegrated rivals, therefore posing no risk of impeding entry. They further argued that vertical deals would not affect a firm’s pricing and output policies, the primary metrics in their analysis. Under this framework, only horizontal mergers affect competition, as “[h]orizontal mergers increase market share, but vertical mergers do not.”129

Chicago School theory holds that concerns about both leverage and foreclosure are misguided. Under the “single monopoly profit theorem,” the amount of profit that a firm can extract from one market is fixed and cannot be expanded through extending into an adjacent market if the two products are used in fixed proportions.130 Under this premise, not only does monopoly leveraging not pose any competitive concern, but—since it can only be motivated by efficiencies, not profits—it is actually procompetitive when it does occur.

The traditional worries about foreclosure, Bork claimed, were unfounded, as “[p]redation through vertical merger is extremely unlikely.”131 A manufacturer would not favor its retail subsidiary over others unless it was cheaper to do so—in which case, Bork argued, discriminating would yield efficiencies that the firm would pass on to consumers. Additionally, any manufacturer that sought to privilege its own retailer would face “entrants who would arrive in sky-darkening swarms for the profitable alternatives.”132 In other words, Bork’s take was that vertical integration generally would not create forms of market power that firms could use to hike prices or constrain output. In the rare case that vertical integration did create this form of market power, he believed that it would be disciplined by actual or potential entry by competitors.133 In light of this, antitrust law’s aversion to vertical arrangements was, Bork argued, irrational. “The law against vertical mergers is merely a law against the creation of efficiency.”134

With the election of President Reagan, this view of vertical integration became national policy. In 1982 and 1984, the Department of Justice (DOJ) and the FTC issued new merger guidelines outlining the framework that officials would use when reviewing horizontal deals.135 The 1984 version included guidelines specific to vertical deals.136 Part of a sweeping effort to overhaul antitrust enforcement, the new guidelines narrowed the circumstances in which the agencies would challenge vertical mergers.137 Although the guidelines acknowledged that vertical mergers could sometimes give rise to competitive concerns, in practice the change constituted a de facto approval of vertical deals. The DOJ and FTC did not challenge even one vertical merger during President Reagan’s tenure.138

Although subsequent administrations have continued reviewing vertical mergers, the Chicago School’s view that these deals generally do not pose threats to competition has remained dominant.139 Rejection of vertical tie-ups—standard through the 1960s and 1970s—is extremely rare today;140 in instances where agencies spot potential harm, they tend to impose conduct remedies or require divestitures rather than block the deal outright.141 The Obama Administration took this approach with two of the largest vertical deals of the last decade: Comcast/NBC and Ticketmaster/LiveNation. In each case, consumer advocates opposed the deal142 and warned that the tie-up would concentrate significant power in the hands of a single company,143 which it could use to engage in exclusionary practices, hike prices for consumers, and dock payments to content producers, such as TV screenwriters and musicians. Nonetheless, the DOJ attached certain behavioral conditions and required a minor divestiture, ultimately approving both deals.144 The district court held the consent decrees to be in the public interest.

II. Why competitive process and structure matter

The current framework in antitrust fails to register certain forms of anticompetitive harm and therefore is unequipped to promote real competition—a shortcoming that is illuminated and amplified in the context of online platforms and data-driven markets. This failure stems both from assumptions embedded in the Chicago School framework and from the way this framework assesses competition.

Notably, the present approach fails even if one believes that antitrust should promote only consumer interests. Critically, consumer interests include not only cost but also product quality, variety, and innovation. Protecting these long-term interests requires a much thicker conception of “consumer welfare” than what guides the current approach. But more importantly, the undue focus on consumer welfare is misguided. It betrays legislative history, which reveals that Congress passed antitrust laws to promote a host of political economic ends—including our interests as workers, producers, entrepreneurs, and citizens. It also mistakenly supplants a concern about process and structure (i.e., whether power is sufficiently distributed to keep markets competitive) with a calculation regarding outcome (i.e., whether consumers are materially better off).

Antitrust law and competition policy should promote not welfare but competitive markets. By refocusing attention back on process and structure, this approach would be faithful to the legislative history of major antitrust laws. It would also promote actual competition—unlike the present framework, which is overseeing concentrations of power that risk precluding real competition.

A. Price and Output Do Not Cover the Full Range of Threats to Consumer Welfare

As discussed in Part I, modern doctrine assumes that advancing consumer welfare is the sole purpose of antitrust. But the consumer welfare approach to antitrust is unduly narrow and betrays congressional intent, as evident from legislative history and as documented by a vast body of scholarship. I argue in this Note that the rise of dominant internet platforms freshly reveals the shortcomings of the consumer welfare framework and that it should be abandoned.

Strikingly, the current approach fails even if one believes that consumer interests should remain paramount.Focusing primarily on price and output undermines effective antitrust enforcement by delaying intervention until market power is being actively exercised, and largely ignoring whether and how it is being acquired. In other words, pegging anticompetitive harm to high prices and/or lower output—while disregarding the market structure and competitive process that give rise to this market power—restricts intervention to the moment when a company has already acquired sufficient dominance to distort competition.

This approach is misguided because it is much easier to promote competition at the point when a market risks becoming less competitive than it is at the point when a market is no longer competitive. The antitrust laws reflect this recognition, requiring that enforcers arrest potential restraints to competition “in their incipiency.”145 But the Chicago School’s hostility to false positives—and insistence that market power and high concentration both reflect and generate efficiency146—has undermined this incipiency standard and enfeebled enforcement as a whole. Indeed, enforcers have largely abandoned section 2 monopolization claims,147 which—by virtue of assessing how a single company amasses and exercises its power—traditionally involved an inquiry into structure. By instead relying primarily on price and output effects as metrics of competition, enforcers risk overlooking the structural weakening of competition until it becomes difficult to address effectively, an approach that undermines consumer welfare.

Indeed, growing evidence shows that the consumer welfare frame has led to higher prices and few efficiencies, failing by its own metrics.148 It arguably has further contributed to a decline in new business growth, resulting in reduced opportunities for entrepreneurs and a stagnant economy.149 The long-term interests of consumers include product quality, variety, and innovation—factors best promoted through both a robust competitive process and open markets. By contrast, allowing a highly concentrated market structure to persist endangers these long-term interests, since firms in uncompetitive markets need not compete to improve old products or tinker to create news ones. Even if we accept consumer welfare as the touchstone of antitrust, ensuring a competitive process—by looking, in part, to how a market is structured—ought to be key. Empirical studies revealing that the consumer welfare frame has resulted in higher prices—failing even by its own terms—support the need for a different approach.

B. Antitrust Laws Promote Competition To Serve a Variety of Interests

Legislative history reveals that the idea that “Congress designed the Sherman Act as a ‘consumer welfare prescription’”150 is wrong.151 Congress enacted antitrust laws to rein in the power of industrial trusts, the large business organizations that had emerged in the late nineteenth century. Responding to a fear of concentrated power, antitrust sought to distribute it. In this sense, antitrust was “guided by principles.”152 The law was “for diversity and access to markets; it was against high concentration and abuses of power.”153

More relevant than any single goal was this general vision. When Congress passed the Sherman Act in 1890, Senator John Sherman called it “a bill of rights, a charter of liberty,” and stressed its importance in political terms.154On the floor of the Senate he declared,

If we will not endure a king as a political power, we should not endure a king over the production, transportation, and sale of any of the necessities of life. If we would not submit to an emperor, we should not submit to an autocrat of trade, with power to prevent competition and to fix the price of any commodity.”155

In other words, what was at stake in keeping markets open—and keeping them free from industrial monarchs—was freedom.

Animating this vision was the understanding that concentration of economic power also consolidates political power, “breed[ing] antidemocratic political pressures.”156 This would occur through enabling a small minority to amass outsized wealth, which they could then use to influence government. But it would also occur by permitting “private discretion by a few in the economic sphere” to “control[] the welfare of all,” undermining individual and business freedom.157 In the lead up to the passage of the Sherman Act, Senator George Hoar warned that monopolies were “a menace to republican institutions themselves.”158

This vision encompassed a variety of ends. For one, competition policy would prevent large firms from extracting wealth from producers and consumers in the form of monopoly profits.159 Senator Sherman, for example, described overcharges by monopolists as “extortion which makes the people poor,”160 while Senator Richard Coke referred to them as “robbery.”161 Representative John Heard announced that trusts had “stolen millions from the people,”162 and Congressman Ezra Taylor noted that the beef trust “robs the farmer on the one hand and the consumer on the other.”163 In the words of Senator James George, “[t]hey aggregate to themselves great enormous wealth by extortion which makes the people poor.”164

Notably, this focus on wealth transfers was not solely economic. Leading up to the passage of the Sherman Act, price levels in the United States were stable or slowly decreasing.165 If the exclusive concern had been higher prices, then Congress could have focused on those industries where prices were, indeed, high or still rising. The fact that Congress chose to denounce unjust redistribution suggests that something else was at play—namely, that the public was “angered less by the reduction in their wealth than by the way in which the wealth was extracted.”166 In other words, though the harm was being registered through an economic effect—a wealth transfer—the underlying source of the grievance was also political.167

Another distinct goal was to preserve open markets, in order to ensure that new businesses and entrepreneurs had a fair shot at entry. Several Congressmen advocated for the Federal Trade Commission Act because it would help promote small business. Senator James Reed expressly noted that Congress’s aim in passing the law was to keep markets open to independent firms.168 When discussing the Sherman Act, Senator George lamented that if large-scale industry were allowed to grow unchecked, it would “crush out all small men, all small capitalists, all small enterprises.”169

Through the 1950s, courts and enforcers applied antitrust laws to promote this variety of aims. While the vigor and tenor of enforcement varied, there was an overarching understanding that antitrust served to protect what Justice Louis Brandeis called “industrial liberty.”170 Key to this vision was the recognition that excessive concentrations of private power posed a public threat, empowering the interests of a few to steer collective outcomes. “Power that controls the economy should be in the hands of elected representatives of the people, not in the hands of an industrial oligarchy,” Justice William O. Douglas wrote.171 Decentralizing this power would ensure that “the fortunes of the people will not be dependent on the whim or caprice, the political prejudice, the emotional stability of a few self-appointed men.”172

As described in Part I, Chicago School scholars upended this traditional approach, concluding that the only legitimate goal of antitrust is consumer welfare, best promoted through enhancing economic efficiency. Notably, some prominent liberals—including John Kenneth Galbraith—ratified this idea, championing centralization.173 In the wake of high inflation in the 1970s, Ralph Nader and other consumer advocates also came to support an antitrust regime centered on lower prices, according with the Chicago School’s view.174 By orienting antitrust toward material rather than political ends, both the neoclassical school and its critics effectively embraced concentration over competition.175

Focusing antitrust exclusively on consumer welfare is a mistake.176 For one, it betrays legislative intent, which makes clear that Congress passed antitrust laws to safeguard against excessive concentrations of economic power. This vision promotes a variety of aims, including the preservation of open markets, the protection of producers and consumers from monopoly abuse, and the dispersion of political177 and economic control.178 Secondly, focusing on consumer welfare disregards the host of other ways that excessive concentration can harm us—enabling firms to squeeze suppliers and producers, endangering system stability (for instance, by allowing companies to become too big to fail),179 or undermining media diversity,180 to name a few. Protecting this range of interests requires an approach to antitrust that focuses on the neutrality of the competitive process and the openness of market structures.

C.Promoting Competition Requires Analysis of Process and Structure

The Chicago School’s embrace of consumer welfare as the sole goal of antitrust is problematic for at least two reasons. First, as described in Section II.B, this idea contravenes legislative history, which shows that Congress passed antitrust laws to safeguard against excessive concentrations of private power. It recognized, in turn, that this vision would protect a host of interests, which the sole focus on “consumer welfare” disregards. Second, by adopting this new goal, the Chicago School shifted the analytical emphasis away from process—the conditions necessary for competition—and toward an outcome—namely, consumer welfare.181 In other words, a concern about structure (is power sufficiently distributed to keep markets competitive?) was replaced by a calculation (did prices rise?).182 This approach is inadequate to promote real competition, a failure that is amplified in the case of dominant online platforms.

Antitrust doctrine has evolved to reflect this redefinition. The recoupment requirement in predatory pricing, for example, reflects the idea that competition is harmed only if the predator can ultimately charge consumers supracompetitive prices.183 This logic is agnostic about process and structure; it measures the health of competition primarily through effects on price and output. The same is true in the case of vertical integration. The modern view of integration largely assumes away barriers to entry, an element of structure, presuming that any advantages enjoyed by the integrated firm trace back to efficiencies.184

More generally, modern doctrine assumes that market power is not inherently harmful and instead may result from and generate efficiencies. In practice, this presumes that market power is benign unless it leads to higher prices or reduced output—again glossing over questions about the competitive process in favor of narrow calculations.185 In other words, this approach equates harm entirely with whether a firm chooses to exercise its market power through price-based levers, while disregarding whether a firm has developed this power, distorting the competitive process in some other way.186 But allowing firms to amass market power makes it more difficult to meaningfully check that power when it is eventually exercised. Companies may exploit their market power in a host of competition-distorting ways that do not directly lead to short-term price and output effects.

I propose that a better way to understand competition is by focusing on competitive process and market structure.187 By arguing for a focus on market structure, I am not advocating a strict return to the structure-conduct-performance paradigm. Instead, I claim that seeking to assess competition without acknowledging the role of structure is misguided. This is because the best guardian of competition is a competitive process, and whether a market is competitive is inextricably linked to—even if not solely determined by—how that market is structured. In other words, an analysis of the competitive process and market structure will offer better insight into the state of competition than do measures of welfare.

Moreover, this approach would better protect the range of interests that Congress sought to promote through preserving competitive markets, as described in Section II.B. Foundational to these interests is the distribution of ownership and control—inescapably a question of structure. Promoting a competitive process also minimizes the need for regulatory involvement. A focus on process assigns government the task of creating background conditions, rather than intervening to manufacture or interfere with outcomes.188

In practice, adopting this approach would involve assessing a range of factors that give insight into the neutrality of the competitive process and the openness of the market. These factors include: (1) entry barriers, (2) conflicts of interest, (3) the emergence of gatekeepers or bottlenecks, (4) the use of and control over data, and (5) the dynamics of bargaining power. An approach that took these factors seriously would involve an assessment of how a market is structured and whether a single firm had acquired sufficient power to distort competitive outcomes.189 Key questions involving these factors would be: What lines of business is a firm involved in and how do these lines of business interact? Does the structure of the market create or reflect dependencies? Has a dominant player emerged as a gatekeeper so as to risk distorting competition?

Attention to structural concerns and the competitive process are especially important in the context of online platforms, where price-based measures of competition are inadequate to capture market dynamics, particularly given the role and use of data.190 As internet platforms mediate a growing share of both communications and commercial activity, ensuring that our framework fits how competition actually works in these markets is vital. Below I document facets of Amazon’s power, trace the source of its growth, and analyze the effects of its dominance. Doing so through the lens of structure and process enables us to make sense of the company’s strategy and illuminates anticompetitive aspects of its business.

III. Amazon’s Business Strategy

Amazon has established dominance as an online platform thanks to two elements of its business strategy: a willingness to sustain losses and invest aggressively at the expense of profits, and integration across multiple business lines.191 These facets of its strategy are independently significant and closely interlinked—indeed, one way it has been able to expand into so many areas is through foregoing returns. This strategy—pursuing market share at the expense of short-term returns—defies the Chicago School’s assumption of rational, profit-seeking market actors. More significantly, Amazon’s choice to pursue heavy losses while also integrating across sectors suggests that in order to fully understand the company and the structural power it is amassing, we must view it as an integrated entity. Seeking to gauge the firm’s market role by isolating a particular line of business and assessing prices in that segment fails to capture both (1) the true shape of the company’s dominance and (2) the ways in which it is able to leverage advantages gained in one sector to boost its business in another.

A. Willingness To Forego Profits To Establish Dominance

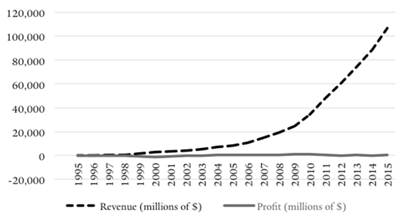

Recently, Amazon has started reporting consistent profits, largely due to the success of Amazon Web Services, its cloud computing business.192 Its North America retail business runs on much thinner margins, and its international retail business still runs at a loss.193 But for the vast majority of its twenty years in business, losses—not profits—were the norm. Through 2013, Amazon had generated a positive net income in just over half of its financial reporting quarters. Even in quarters in which it did enter the black, its margins were razor-thin, despite astounding growth. The graph below captures the general trend.

Figure 1.

Amazon’s Profits194

Just as striking as Amazon’s lack of interest in generating profit has been investors’ willingness to back the company.195 With the exception of a few quarters in 2014, Amazon’s shareholders have poured money in despite the company’s penchant for losses. On a regular basis, Amazon would report losses, and its share price would soar.196 As one analyst told the New York Times, “Amazon’s stock price doesn’t seem to be correlated to its actual experience in any way.”197

Analysts and reporters have spilled substantial ink seeking to understand the phenomenon. As one commentator joked in a widely circulated post, “Amazon, as best I can tell, is a charitable organization being run by elements of the investment community for the benefit of consumers.”198

In some ways, the puzzlement is for naught: Amazon’s trajectory reflects the business philosophy that Bezos outlined from the start. In his first letter to shareholders, Bezos wrote:

We believe that a fundamental measure of our success will be the shareholder value we create over the long term. This value will be a direct result of our ability to extend and solidify our current market leadership position . . . . We first measure ourselves in terms of the metrics most indicative of our market leadership: customer and revenue growth, the degree to which our customers continue to purchase from us on a repeat basis, and the strength of our brand. We have invested and will continue to invest aggressively to expand and leverage our customer base, brand, and infrastructure as we move to establish an enduring franchise.199

In other words, the premise of Amazon’s business model was to establish scale. To achieve scale, the company prioritized growth. Under this approach, aggressive investing would be key, even if that involved slashing prices or spending billions on expanding capacity, in order to become consumers’ one-stop-shop. This approach meant that Amazon “may make decisions and weigh tradeoffs differently than some companies,” Bezos warned.200 “At this stage, we choose to prioritize growth because we believe that scale is central to achieving the potential of our business model.”201

The insistent emphasis on “market leadership” (Bezos relies on the term six times in the short letter)202 signaled that Amazon intended to dominate. And, by many measures, Amazon has succeeded. Its year-on-year revenue growth far outpaces that of other online retailers.203 Despite efforts by big-box competitors like Walmart, Sears, and Macy’s to boost their online operations, no rival has succeeded in winning back market share.204

One of the primary ways Amazon has built a huge edge is through Amazon Prime, the company’s loyalty program, in which Amazon has invested aggressively. Initiated in 2005, Amazon Prime began by offering consumers unlimited two-day shipping for $79.205 In the years since, Amazon has bundled in other deals and perks, like renting e-books and streaming music and video, as well as one-hour or same-day delivery. The program has arguably been the retailer’s single biggest driver of growth.206 Amazon does not disclose the exact number of Prime subscribers, but analysts believe the number of users has reached 63 million—19 million more than in 2015.207 Membership doubled between 2011 and 2013; analysts expect it to “easily double again by 2017.”208 By 2020, it is estimated that half of U.S. households may be enrolled.209

As with its other ventures, Amazon lost money on Prime to gain buy-in. In 2011 it was estimated that each Prime subscriber cost Amazon at least $90 a year—$55 in shipping, $35 in digital video—and that the company therefore took an $11 loss annually for each customer.210 One Amazon expert tallies that Amazon has been losing $1 billion to $2 billion a year on Prime memberships.211 The full cost of Amazon Prime is steeper yet, given that the company has been investing heavily in warehouses, delivery facilities, and trucks, as part of its plan to speed up delivery for Prime customers—expenditures that regularly push it into the red.212

Despite these losses—or perhaps because of them—Prime is considered crucial to Amazon’s growth as an online retailer. According to analysts, customers increase their purchases from Amazon by about 150% after they become Prime members.213 Prime members comprise 47% of Amazon’s U.S. shoppers.214 Amazon Prime members also spend more on the company’s website—an average of $1,500 annually, compared to $625 spent annually by non-Prime members.215 Business experts note that by making shipping free, Prime “successfully strips out paying for . . . the leading consumer burden of online shopping.”216 Moreover, the annual fee drives customers to increase their Amazon purchases in order to maximize the return on their investment.217

As a result, Amazon Prime users are both more likely to buy on its platform and less likely to shop elsewhere. “[Sixty-three percent] of Amazon Prime members carry out a paid transaction on the site in the same visit,” compared to 13% of non-Prime members.218 For Walmart and Target, those figures are 5% and 2% respectively.219 One study found that less than 1% of Amazon Prime members are likely to consider competitor retail sites in the same shopping session. Non-Prime members, meanwhile, are eight times more likely than Prime members to shop between both Amazon and Target in the same session.220 In the words of one former Amazon employee who worked on the Prime team, “It was never about the $79. It was really about changing people’s mentality so they wouldn’t shop anywhere else.”221 In that regard, Amazon Prime seems to have proven successful.222

In 2014, Amazon hiked its Prime membership fee to $99.223 The move prompted some consumer ire, but 95% of Prime members surveyed said they would either definitely or probably renew their membership regardless,224 suggesting that Amazon has created significant buy-in and that no competitor is currently offering a comparably valuable service at a lower price. It may, however, also reveal the general stickiness of online shopping patterns. Although competition for online services may seem to be “just one click away,” research drawing on behavioral tendencies shows that the “switching cost” of changing web services can, in fact, be quite high.225

No doubt, Amazon’s dominance stems in part from its first-mover advantage as a pioneer of large-scale online commerce. But in several key ways, Amazon has achieved its position through deeply cutting prices and investing heavily in growing its operations—both at the expense of profits. The fact that Amazon has been willing to forego profits for growth undercuts a central premise of contemporary predatory pricing doctrine, which assumes that predation is irrational precisely because firms prioritize profits over growth.226 In this way, Amazon’s strategy has enabled it to use predatory pricing tactics without triggering the scrutiny of predatory pricing laws.

B. Expansion into Multiple Business Lines

Another key element of Amazon’s strategy—and one partly enabled by its capacity to thrive despite posting losses—has been to expand aggressively into multiple business lines.227 In addition to being a retailer, Amazon is a marketing platform, a delivery and logistics network, a payment service, a credit lender, an auction house, a major book publisher, a producer of television and films, a fashion designer, a hardware manufacturer, and a leading provider of cloud server space and computing power.228 For the most part, Amazon has expanded into these areas by acquiring existing firms.229

Involvement in multiple, related business lines means that, in many instances, Amazon’s rivals are also its customers. The retailers that compete with it to sell goods may also use its delivery services, for example, and the media companies that compete with it to produce or market content may also use its platform or cloud infrastructure. At a basic level this arrangement creates conflicts of interest, given that Amazon is positioned to favor its own products over those of its competitors.

Critically, not only has Amazon integrated across select lines of business, but it has also emerged as central infrastructure for the internet economy. Reports suggest this was part of Bezos’s vision from the start. According to early Amazon employees, when the CEO founded the business, “his underlying goals were not to build an online bookstore or an online retailer, but rather a ‘utility’ that would become essential to commerce.”230 In other words, Bezos’s target customer was not only end-consumers but also other businesses.

Amazon controls key critical infrastructure for the Internet economy—in ways that are difficult for new entrants to replicate or compete against. This gives the company a key advantage over its rivals: Amazon’s competitors have come to depend on it. Like its willingness to sustain losses, this feature of Amazon’s power largely confounds contemporary antitrust analysis, which assumes that rational firms seek to drive their rivals out of business. Amazon’s game is more sophisticated. By making itself indispensable to e-commerce, Amazon enjoys receiving business from its rivals, even as it competes with them. Moreover, Amazon gleans information from these competitors as a service provider that it may use to gain a further advantage over them as rivals—enabling it to further entrench its dominant position.

IV. Establishing Structural Dominance

Amazon now controls 46% of all e-commerce in the United States.231 Not only is it the fastest-growing major retailer, but it is also growing faster than e-commerce as a whole.232 In 2010, it employed 33,700 workers; by June 2016, it had 268,900.233 It is enjoying rapid success even in sectors that it only recently entered. For example, the company “is expected to triple its share of the U.S. apparel market over the next five years.”234 Its clothing sales recently rose by $1.1 billion—even as online sales at the six largest U.S. department stores fell by over $500 million.235

These figures alone are daunting, but they do not capture the full extent of Amazon’s role and power. Amazon’s willingness to sustain losses and invest aggressively at the expense of profits, coupled with its integration across sectors, has enabled it to establish a dominant structural role in the market.

In the Sections that follow, I describe several examples of Amazon’s conduct that illustrate how the firm has established structural dominance.236 These examples—its handling of e-books and its battle with an independent online retailer—focus on predatory pricing practices. These cases suggest ways in which Amazon may benefit from predatory pricing even if the company does not raise the price of the goods on which it lost money. The other examples, Fulfillment-by-Amazon and Amazon Marketplace, demonstrate how Amazon has become an infrastructure company, both for physical delivery and e-commerce, and how this vertical integration implicates market competition. These cases highlight how Amazon can use its role as an infrastructure provider to benefit its other lines of business. These examples also demonstrate how high barriers to entry may make it difficult for potential competitors to enter these spheres, locking in Amazon’s dominance for the foreseeable future. All four of these accounts raise concerns about contemporary antitrust’s ability to register and address the anticompetitive threat posed by Amazon and other dominant online platforms.

A. Below-Cost Pricing of Bestseller E-Books and the Limits of Modern Recoupment Analysis

Amazon entered the e-book market by pricing bestsellers below cost. Although this strategic pricing helped Amazon to establish dominance in the e-book market, the government perceived Amazon’s cost cutting as benign, focusing on the profitability of e-books in the aggregate and characterizing the company’s pricing of bestsellers as “loss leading” rather than predatory pricing. This failure to recognize Amazon’s conduct as anticompetitive stems from a misunderstanding of online markets generally and of Amazon’s strategy specifically. Additionally, analyzing the issues raised in this case suggests that Amazon could recoup its losses through means not captured by current antitrust analysis.

In late 2007, Amazon rolled out the Kindle, its e-reading device, and launched a new e-book library.237 Before introducing the device, CEO Jeff Bezos had decided to price bestseller e-books at $9.99,238 significantly below the $12 to $30 that a new hardback typically costs.239 Critically, the wholesale price at which Amazon was buying books from publishers had not dropped; it was instead choosing to price e-books below cost.240 Analysts estimate that Amazon sold the Kindle device below manufacturing cost too.241 Bezos’s plan was to dominate the e-book selling business in the way that Apple had become the go-to platform for digital music.242 The strategy worked: through 2009, Amazon dominated the e-book retail market, selling around 90% of all e-books.243

Publishers, fearing that Amazon’s $9.99 price point for e-books would permanently drive down the price that consumers were willing to pay for all books, sought to wrest back some control. When the opportunity came to partner with Apple to sell e-books through the iBookstore store, five of the “Big Six” publishers introduced agency pricing, whereby publishers would set the final retail price and Apple would get a 30% cut.244 After securing this deal, MacMillan, one of the “Big Six,” demanded that Amazon, too, adopt this pricing model.245 Though it initially refused and delisted MacMillan’s books,246 Amazon ultimately relented, explaining to readers that “we will have to capitulate and accept Macmillan’s terms because Macmillan has a monopoly over their own titles.”247 Other publishers followed suit, halting Amazon’s ability to price e-books at $9.99.248

In 2012, the DOJ sued the publishers and Apple for colluding to raise e-book prices.249 In response to claims that the DOJ was going after the wrong actor—given that it was Amazon’s predatory tactics that drove the publishers and Apple to join forces—the DOJ investigated Amazon’s pricing strategies and found “persuasive evidence lacking” to show that the company had engaged in predatory practices.250 According to the government, “from the time of its launch, Amazon’s e-book distribution business has been consistently profitable, even when substantially discounting some newly released and bestselling titles.”251

Judge Cote, who presided over the district court trial, refrained from affirming the government’s conclusion.252 Still, the government’s argument illustrates the dominant framework that courts and enforcers use to analyze predation—and how it falls short. Specifically, the government erred by analyzing the profitability of Amazon’s e-book business in the aggregate and by characterizing the conduct as “loss leading” rather than potentially predatory pricing.253 These missteps suggest a failure to appreciate two critical aspects of Amazon’s practices: (1) how steep discounting by a firm on a platform-based product creates a higher risk that the firm will generate monopoly power than discounting on non-platform goods and (2) the multiple ways Amazon could recoup losses in ways other than raising the price of the same e-books that it discounted.

On the first point, the government argued that Amazon was not engaging in predation because in the aggregate,Amazon’s e-books business was profitable. This perspective overlooks how heavy losses on particular lines of e-books (bestsellers, for example, or new releases) may have thwarted competition, even if the e-books business as a whole was profitable. That the DOJ chose to define the relevant market as e-books—rather than as specific lines, like bestseller e-books—reflects a deeper mistake: the failure to recognize how the economics of platform-based products differ in crucial ways from non-platform goods. 254 As a result, the DOJ analyzed the e-book market as it would the market for physical books.